Meat exports, which are important for the U.S. agricultural sector, have more than doubled in the past 4 decades, increasing from $13.5 billion (in 2022 prices) in 1980 to $32.4 billion in 2022 (USDA, 2023). The United States plays an important role as a supplier of beef, pork, and chicken to the global market, and a substantial portion of U.S. meat exports are destined for Asian markets, including South Korea (representing 8% of U.S. meat exports in 2022), Japan (11%), China/Hong Kong (10%), and Taiwan (4%) (USDA, 2022). However, there is potential for expanded U.S. exports to Asia, including increased meat exports to the 10 member countries of the Association of Southeast Asian Nations (ASEAN). Future export growth for U.S. meat depends on income growth of importing countries, competitiveness of U.S. products, and access to global markets. Trade barriers, such as import tariffs, hamper U.S. exports. Even though the average tariff rates on imports into ASEAN countries decreased from 9% in 2000 to 4.5% in 2015, nontariff measures (NTMs)— mostly related to sanitary and phytosanitary (SPS) measures and technical barriers to trade—increased from 1,634 to 5,975 measures over the same period (UNCTAD, 2016). Although ASEAN established several preferential trade agreements, trade barriers remain on agricultural products, and there is no trade agreement between the United States and ASEAN (Beckman, Gopinath, and Daugherty, 2021). This article examines the ASEAN meat import market and the potential for increased U.S. meat exports to ASEAN resulting from tariff removal for animal products.

Economic growth in Southeast Asia has been strong in the past decade. Income levels have been rising with the accelerated development of the region, leading to an increase in protein-based diets (OECD and FAO, 2017). The increasing demand for animal protein in ASEAN presents opportunities for U.S. suppliers to increase meat exports to the region (Lee and Jones,2023). ASEAN is both strategically and economically important for the United States. ASEAN has become oneof the most important players in the global trading system and represents the world’s fifth largest economy (Elms, 2020). In addition, all ASEAN countries are projected to increase consumption of pork and poultry, especially over the next decade, representing potential for increased meat imports, which could be supplied by the United States (Petri and Plummer, 2014; Lee and Hansen, 2019). ASEAN has strong relationships and free trade agreements (FTA) with China, Hong Kong, South Korea, Japan, India, Australia, and New Zealand and is a member of the 15-country Regional Comprehensive Economic Partnership. Meanwhile, the United States does not have important free trade agreements with countries in the region, except for an FTA with Singapore. The lack of trade policy commitments in the region are likely to hamper U.S. export potential in the future and may limit U.S. competitiveness in the ASEAN meat import market.

This article explores ASEAN export potential for U.S. meat by providing a detailed trade profile for ASEAN meat import sourcing for beef, pork, and poultry. We discuss the tariff and nontariff barriers that impede U.S. meat exports in the region and focus on the U.S. productive capacity to meet the growing demands for animal products in Southeast Asia. This article is an important contribution given the importance of U.S. meat export potential in the Southeast Asia region. The competitiveness of U.S. meat in Southeast Asian export markets is continually highlighted by agriculturalists as a key agricultural trade policy priority (Ufer, Padilla, and Link, 2023).

The ASEAN Free Trade Area (AFTA) is formed by the 10 ASEAN members. AFTA reduced tariffs and removed quantitative restrictions and other nontariff barriers through a common effective preferential tariff among ASEAN countries, aiming to increase ASEAN economic growth. Outside of AFTA, ASEAN also facilitated liberalization with China, Japan, South Korea, Australia, India, and New Zealand. Both the United States and the European Union (EU) have free trade agreements with Singapore but not with the other ASEAN member countries.

Meat consumption dynamics are changing substantially in ASEAN due to the pace of economic development of the region, demonstrating the potential for increased animal product exports to the region. However, opening ASEAN markets to imports is not so simple. ASEAN members impose different types of constraints on imports, especially food imports. Thailand imposes the largest number of SPS measures on imports (282 SPS measures), followed by the Philippines (150), Indonesia (144), Malaysia (88), and Vietnam (83). Singapore and Brunei have a moderate number of SPS measures, while Cambodia, Laos, and Myanmar have the lowest number of SPS measures in ASEAN. Since 2009, NTMs were imposed specifically on beef, pork, and poultry imports from the United States and other countries by Indonesia (24 NTMs), Vietnam (18), Malaysia (14), the Philippines (13), Laos (11), Myanmar (9), Cambodia (6), and Thailand (4) (UNCTAD, 2023). NTMs are policy measures that can potentially have an economic effect on international trade, changing the quantities and/or prices of goods traded. NTMs consist of mandatory requirements, rules, or regulations that are legally established by countries. Examples of NTMs include technical barriers to trade, SPS measures, certification, quotas, imports and export licenses, and rules of origin.

Despite trade barriers, ASEAN countries have become increasingly important meat importers. Expanded demand for meat in the region has been driven by urbanization, improved standards of living, and changes in dietary preferences of the region’s ascending urban middle-class (Lee and Hansen, 2019). In addition, the Russia–Ukraine conflict reduced the global supply of feed, which ASEAN countries depend on for livestock production. Consequently, ASEAN meat production was negatively affected, creating an increased need for meat imports among ASEAN members. Beef and pork production in ASEAN countries decreased by -5% and -4.6%, respectively, between 2017 and 2021, while poultry production increased by a meager 1.5% in the same period (FAO, 2023). At the same time, ASEAN pork imports increased by 27% from 2017 to 2021, largely as a result of augmented pork imports by Cambodia, Vietnam, and Thailand. Poultry imports in ASEAN increased by 5% in the same period, led by Thailand, the Philippines, and Cambodia. Beef imports decreased by -4.9% between 2017 and 2021. However, disaggregated data at the country level shows that Cambodia increased beef imports by 45%, Indonesia by 20%, the Philippines by 14%, and Thailand by 12% in that period (UN Statistics Division, 2023).

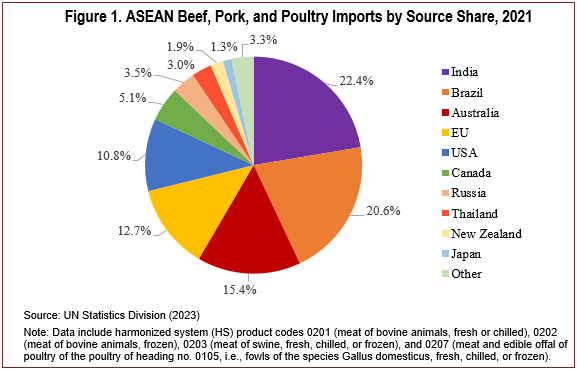

ASEAN members combined imported $2.9 billion of beef, $1.2 billion of pork, and $1.2 billion of poultry in 2021, representing 5% of total world imports of both beef and poultry and 3.5% of world pork imports in that year. Figure 1 shows the share of the 10 main exporters of meat to ASEAN. India, Brazil, and Australia comprise almost 60% of total ASEAN imports of beef, pork, and poultry. Approximately 22% of ASEAN imports of meat come from India, followed by nearly 21% from Brazil. The United States represents approximately 11% of ASEAN imports, behind Australia with a share of 15% and the EU with 13%. India represented 41% of ASEAN beef imports in 2021, while Australia’s share was 26%, followed by Brazil (14%) and the United States (7%). Five ASEAN members concentrated 94% of the region’s beef imports in the same year: Indonesia (27%), Malaysia (20%), Vietnam (19%), the Philippines (18%), and Singapore (10%). The EU was the largest source of ASEAN pork imports in 2021, representing 36% of the region’s total pork imports. The other sources of pork in ASEAN were Brazil, with a 22% share, followed by Russia (14%), Canada (13%), and the United States (9%). Pork imports within the region are relatively more concentrated compared to beef imports. The Philippines imported 39% of ASEAN total pork imports, while Vietnam’s and Singapore’s share were 31% and 25%, respectively. Brazil represented 36% of ASEAN poultry imports in 2021, followed by the United States (23%), EU (11%), and China (5%). Approximately 98% of ASEAN poultry imports in 2021 were concentrated in four countries: the Philippines (38%), Singapore (24%), Vietnam (20%), and Malaysia (16%).

The United States faces several challenges to export meat to ASEAN countries. First, customers are spread across many small countries, making it harder to connect exporters to buyers. Second, besides the geographical challenge, import requirements vary widely from country to country. A great number of tariff and nontariff barriers imposed by ASEAN countries, which are established by the government agencies of each country, are related to animal products (UNCTAD, 2016). The United States faces some of the largest tariffs on agricultural product exports to ASEAN, especially for exports of pork (19.1%), other meat (15.8%), and beef (8.7%) (Beckman, Gopinath, and Daugherty, 2021).

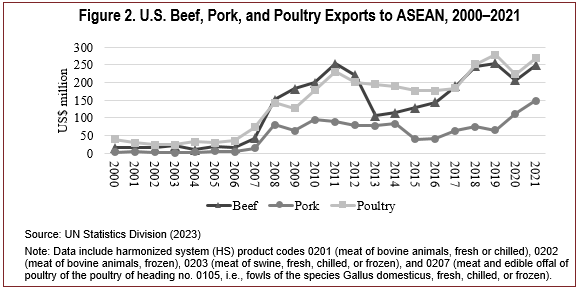

Over the last 2 decades, U.S. meat exports to ASEAN have risen substantially, increasing from $58.7 million in 2000 to $665.7 million in 2021. Figure 2 shows U.S. beef, pork, and poultry exports to ASEAN between 2000 and 2021. However, ASEAN still represents only a small fraction of U.S. exports of meat, highlighting the potential for U.S. exports to the region. Approximately 2.7% of U.S. beef exports in 2021 were destined for ASEAN, valued at $249 million, with 95% being frozen beef and only 5% fresh or chilled beef. Further, 35% of U.S. beef exports to ASEAN in 2021 were destined for Indonesia, while 27% went to the Philippines, 17% to Vietnam, and 15% to Singapore.

U.S. pork exports to ASEAN totaled $148 million in 2021, representing 2.5% of U.S. total pork exports in that year, with 86% destined for the Philippines, 7% to Vietnam, and 6% to Singapore. On the other hand, ASEAN represented 5.6% of U.S. poultry exports in 2021, corresponding to approximately $269 million. 52% of U.S. poultry exports to ASEAN were destined for the Philippines, 37% to Vietnam, and 6% to Singapore in the same year.

Although the United States has reached meat export records to East Asia in recent years, U.S. exports destined for ASEAN have grown move slowly compared to exports to South Korea, China, Hong Kong, Japan, and Taiwan. In fact, South Korea has been the most valuable destination for U.S. meat exports since 2021 as a result of the South Korea–U.S. Free Trade Agreement. This shows how imperative it is for the United States to negotiate trade agreements with ASEAN to improve the meat trade and increase the market share in the region.

The United States can benefit from a free trade agreement with ASEAN, since those countries have been recently pursuing comprehensive economic partnerships with important trade partners (Beckman, Gopinath, and Daugherty, 2021). One of the most comprehensive ASEAN free trade agreements to date is the ASEAN–Australia–New Zealand Free Trade Agreement, which is expected to lead to a sharp increase in ASEAN meat imports from Australia and New Zealand in the coming years (Penh, 2022). Important competitors of the United States, including Australia and New Zealand, have a relatively greater opportunity to export agricultural products to ASEAN countries when the United States is excluded from trade negotiations, resulting in a substantial cost for U.S. agricultural exporters (Heerman, Arita, and Gopinath, 2015).

To investigate the potential for increased U.S. meat exports with improved market access in ASEAN, we simulate complete import tariff removal on meat trade between ASEAN and the United States, employing the GTAP model and version 11 of the GTAP database detailed in Aguiar et al. (2022). The GTAP model represents demand, supply, and trade and is a useful tool for an ex-ante analysis of trade policy (Gilbert, Furusawa, and Scollay, 2017). In the model, producers are assumed to be perfectly competitive cost minimizers, with technology defined as a nested production function, and producers demand intermediate inputs based on prices of inputs and outputs. Consumer demand is described by a constant difference of elasticity demand system, and each region’s representative household is assumed to maximize utility derived from the consumption of market goods and savings subject to a regional income constraint. The 160 regions and 65 sectors represented in the database were aggregated into 13 regions and nine sectors, including five agriculture-related sectors plus two meat sectors (beef and other meat) for this analysis. The scenario assumed complete removal of ASEAN import tariffs on U.S. meat and the complete removal of U.S. import tariffs on ASEAN meat, as could happen in the case of a freetrade agreement between the two economies. The simulations consider a short-run setup (1-year) timeframe.

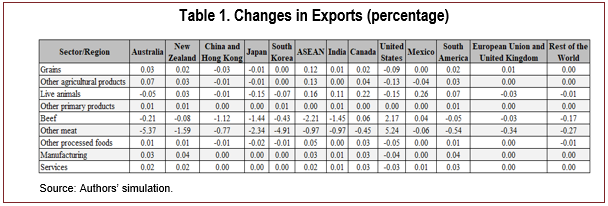

Results show that beef imports would increase by 2.6%, while other meat imports would increase 9.6% in ASEAN. At the same time, U.S. beef exports would increase by 2.17%, and other meat exports by 5.24%. U.S. other meat exports to ASEAN would double, and U.S. beef exports to ASEAN would increase by 67%. With the increase in imports from the United States, ASEAN would decrease beef and other meat imports from other countries by approximately 3.6% and 16%, respectively. U.S. competitors in exports to ASEAN would experience decreases in beef and other meat exports. The most negatively affected in terms of beef exports would be ASEAN (-2.21%), India (-1.45%), and Japan (-1.44%). In terms of other meat exports, Australia and South Korea would be the most negatively affected, with a simulated decrease in other meat exports equal to 5.37% and 4.91%, respectively (Table 1). ASEAN other meat exports would slightly decrease by nearly 1%. In the aggregate, world exports of beef and other meat are simulated to increase by 0.13% and 0.35%, respectively. The international trade of other products is not affected in this scenario as tariffs for trade of other products remain unchained.

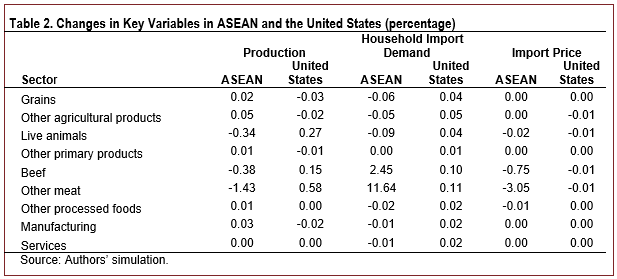

The complete removal of tariffs on the international trade of beef and other meat between ASEAN and the United States would lead to a decrease in ASEAN production of live animals, beef, and other meat production by 0.34%, 0.38%, and 1.43%, respectively. At the same time, U.S. live animal production is simulated to increase by 0.27%, while U.S. beef production would slightly increase by 0.15% and other meat production by 0.58%. ASEAN household demand for imported beef and other meat is simulated to increase by 2.45% and 11.64%, respectively. On the other hand, changes in U.S. household demand for imported beef and other meat would be negligible, increasing by only 0.10%. Commodity prices would not change in the aggregate for this scenario, but import prices in ASEAN would decrease for imports of beef and, especially, for other meat (Table 2).

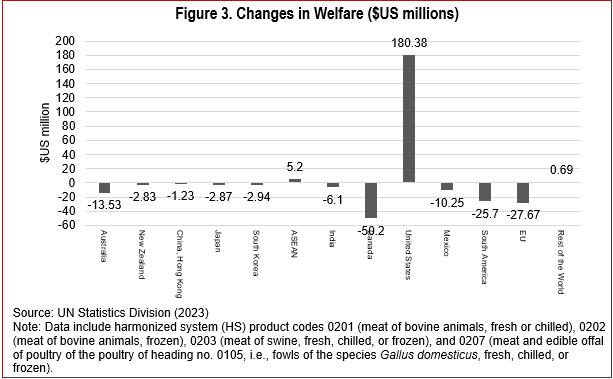

Figure 3 shows the welfare effects from the removal of ASEAN import tariffs on U.S. meat. Welfare is measured by equivalent variation. As expected, the United States is simulated to have the largest gain in welfare equal to $180.4 million, followed by ASEAN, with a $5.2 million increase in welfare. The driver of the welfare increase in ASEAN is changes in allocative efficiency, while the gains from changes in terms of trade is the largest contributor to increased welfare for the United States. Canada presents the highest decrease in welfare (-$50.2 million), followed by the EU (-$27.7 million) and South America (-$25.7 million), resulting from deteriorating terms of trade.

Overall, results show that the United States would benefit from the total removal of import tariffs on meat traded between the United States and ASEAN. On the other hand, ASEAN is simulated to have small decreases in meat production and exports, while beef and other meat import prices would decrease and import volume would increase substantially. The largest U.S. competitors in the ASEAN meat import market, including Australia, EU, and South America would be negatively affected in terms of lost exports and associated decreased welfare. The removal of tariffs would create trade diversion in favor of U.S.-sourced imports at the detriment of imports from other meat suppliers to ASEAN.

Although the United States exports meat to ASEAN, most of the ASEAN import market share for meat-related products is concentrated in other countries, including Australia, Brazil, and the EU. Simulation results show that U.S. beef and other meat exports to ASEAN could increase by 67% and 100%, respectively, when considering the removal of import tariffs on meat traded between the United States and ASEAN. Despite economic shocks and uncertainty during the last 3 years, ASEAN still presents great potential for U.S. meat exports, with no indicators of substantial economic slowdown in the future (Mikic, 2023). The expected accelerating growth of the middle class in ASEAN and corresponding increased meat consumption are also strong indicators of the region’s meat import potential. While results show the market effects from the elimination of import tariffs on meat traded between the United States and ASEAN, there are limitations to this simple analysis. First, tariff reform would include sectors throughout the economy, yet we focus only on the meat sector. Second, tariff reform would likely occur over a phase-in period, and we model immediate tariff removal. Third, the highly aggregated commodity grouping of meat into two sectors, beef and other meat, masks the within-product variation in tariff levels and corresponding magnitudes of changes in tariffs that would occur with an FTA between the two regions. While meat is highly aggregated, this research shows the potential, general implications of tariff reform for the meat market. This article describes the ASEAN meat import market and demonstrates the potential for increased U.S. meat exports to the region with the elimination of ASEAN import tariffs. However, the United States will continue to lose competitiveness in ASEAN without a preferential trade agreement, while U.S. competitors enjoy favorable access to the ASEAN market.