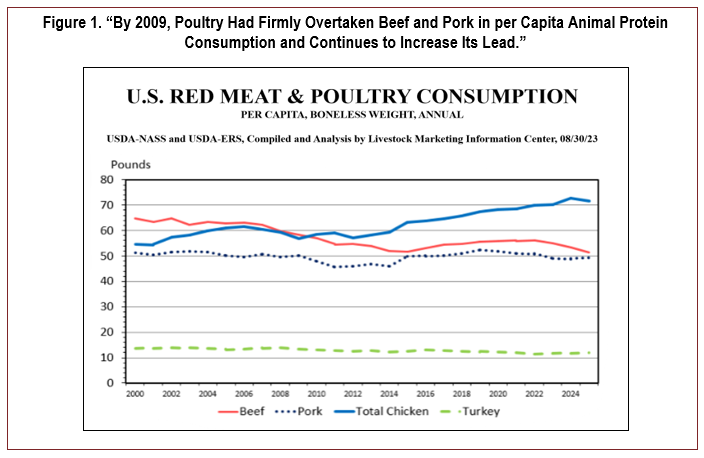

Commercial poultry production is big business. According to the 2017 Farm Census, poultry accounted for over $49 billion in total sales in the United States (U.S. Department of Agriculture, 2023b). National Chicken Council statistics show that broiler production in the United States has sustained an average of 2% growth year over year since 2000, with an estimated 46 billion pounds of ready-to-cook chicken sold in 2022. In the early 2000s, chicken became the most consumed animal protein in the country (Livestock Marketing Information Center, 2023). By 2022, chicken consumption had reached 100 pounds per capita annually, compared to 57 pounds for beef and 51 pounds for pork (National Chicken Council, 2023). Poultry is currently the least expensive animal protein in the United States (U.S. Department of Agriculture, 2023a). The purpose of this paper is not only to further outline some of the reasons for poultry’s rise to prominence but also to explore areas of concern that the industry must address if it is to continue its growth as the preferred animal protein in the United States. The changes that are occurring and are likely to continue—including grower contracts, rising costs of grow-out housing, emerging supply chain issues, and legal concerns—will have profound effects on family farms across the country.

The primary reasons for poultry’s rise to prominence are the low cost of production leading to lower prices and market flexibility, both arising from the vertical integration of the poultry industry. Vertical integration is the consolidation of independent suppliers of various inputs or stages of production into one firm. For instance, the hatchery, feed production, processing plant, transportation, and marketing components required are all owned and operated by a single poultry company. Poultry companies then contract the live grow-out operations to other entities. That is, the chickens, the feed, and the transportation, are all owned and operatedby the poultry companies, while the facilities in which the birds spend their lives growing are owned and operated by independent contract farmers (often called growers). The contract guarantees the grower that the company will supply birds, feed, and management direction while the grower will provide facilities, utilities, and labor to grow the birds. This contract arrangement is beneficial to growers as it allows them to avoid the risk of input commodity price variations and product market fluctuations.

For the contract fee, the companies receive 24/7 bird monitoring by the growers. The growers are the direct providers of bird welfare and environmental control. Proper feed and water access, optimum temperatures, adequate ventilation, and daily mortality management are all necessary to maximize feed efficiency and minimize the cost of production for the company. A typical broiler plant slaughtering 1 million birds per week is served by 50–100 farms operating 300–400 barns. These numbers vary with barn size and barns per farm.

Providing the constant management needed for those facilities would be very expensive and management intensive on company-owned property with company employees. The grow-out contract effectively lowers the cost of production for the company while providing the round-the-clock oversight needed to provide for animal welfare. On the other hand, growers are typically highly leveraged, with high debt relative to income, operating single-use facilities costing over $250,000 per barn, with most farms having four or more barns. Without the birds, feed, supporting facilities, and market development supplied by the integrators, the growers’ businesses would be much more difficult, and riskier, if not impossible. The farmers and the company truly benefit from each other.

Even as this model has been beneficial for many decades in the United States, there have been several developments in recent years that bring the future of this relationship into question. Some of these factors are simple economics, others regulatory, and still others matter of law and litigation.

A primary area of concern is the cost of building new poultry farm facilities. Increasing barn costs have created a housing crunch for the entire industry. In the early 2000s, a broiler farm could be built from the ground up to bird-ready for approximately $10–$12 per square foot of grow-out space. Those farms were typically 80,000–100,000 square foot operations. By the time all the accompanying start-up expenses were added, a typical farm often represented an investment of $1,000,000–$1,500,000. These farms were typically built on a business model utilizing a 15-year loan with the poultry barns expected to have a usable life of at least 25 years. If a grower were financially disciplined, it was very possible to pay the loan off early and enjoy several years of highly profitable operation.

Currently, broiler barns cost between $18–$22 per square foot, with some regions costing more. The increased cost is primarily driven by increases in the costs of materials like lumber, metal, and plastics. Combined with the fact that most farms are now built to capture economies of scale where possible, with larger barns and more barns per site, a typical farm today may have eight or more barns of over 30,000 square feet each on one site, making the farm over twice the size of those built 20 years ago. Labor shortages and increased costs have also played a part for both growers and builders. As farm size has grown, expensive technology is required to allow growers to manage more birds to company standards with less labor. These factors combined have raised the estimated cost of a new eight-barn (33,600 square feet each) farm to almost $6,000,000.

The equity needed to support a loan for such a high capital investment has presented a barrier to many farmers wishing to enter the business. Today, almost all growers must obtain federal loan assistance from the Farm Service Agency or some other assistance to qualify for a poultry farm loan. Loan terms are often lengthened to 20 years to lower annual payments and improve cash flow. Given the high building cost and current average contract pay rates, the simple cash flows for these new farms may still not be enough to support the minimum debt service margin (annual cash available from revenue/annual debt service) of 1.30 that many banking institutions require for a loan.

This has led to poultry companies giving additional building funds directly to the growers to defray the increased building costs and improve cash flows further. These incentives come in many forms, from increased pay rates for defined periods to lump sums at the beginning of a contract to additional cash payments divided over multiple years. These incentives have improved loan availability through better cash flow, but the incentives are temporary in nature. Growers must carefully plan what to do when the incentives run out, and some of the incentives could result in unforeseen tax liabilities.

Often the end of the incentive pay period coincides with depreciation ending for the building and equipment, while at the same time coinciding with maintenance and equipment replacement needs. Longer term loans may leave growers in less than desirable equity positions at a time when they may need to refinance the business to obtain maintenance funding. Therefore, new growers must carefully manage their finances to avoid future problems.

One result of these financial challenges has been an increase in larger multibarn farms owned by business entities and not by family farmers. These large “conglomerate farms” can utilize the financial strengths of investment capital and increased economies of scale by building 20 or more poultry barns at a time, often in multiple locations at once. They hire managers for daily operations, spreading that cost across more barns than the typical family farm would have the ability to do. These larger farms represent both risk and opportunity in many areas. Integrators can potentially benefit from more uniform management across larger numbers of birds, specifically in the areas of biosecurity and basic husbandry. However, there is concentration risk in these same areas. Potentially larger numbers of birds are negatively impacted by poor management on these farms than with the traditional smaller farm model. It is uncertain whether this model will become the norm going forward. The shift seems to be more borne of necessity from grower shortages in some areas rather than the preferred choice of integrators.

The contract grower is a foundational part of the vertically integrated poultry system outlined above, particularly for broiler production. While the contract arrangement removes the production risk of rising feed prices or falling chicken prices from growers, they do face the risks of rising utility costs and rising facility costs. They also operate highly leveraged single-use facilities. Risk often comes with reward opportunities, but that is not true in this case. While the contract grower receives a more predictable return on their investment than a farmer in a more traditional agri-business, they do not get the advantage of potential increased profit due to positive market turns, falling input prices, or forward marketing.

One aspect of these contracts that impacts the predictability of pay for growers has come under scrutiny: the traditional “tournament pay” system of compensation. The tournament pay system evolved as a way for poultry companies to encourage the best management of broiler birds by the independent growers. In short, the system allows for some variability in pay per pound, both positive and negative, of delivered birds based on the actual live production cost to the company. An individual farm’s cost of production is compared to farms with similar birds delivered in the same time frame. This cost of production is made up mostly of feed cost and is commonly called “live-cost.” It is impacted by things such as environmental control at the farm/barn level, feed and water management, and bird mortality. A grower who has an individual live-cost higher than their peers receives lower pay per pound in comparison. This is supported by the argument that much of the resulting live-cost is a direct result of the on-farm management provided by the contract grower. It is also argued the grower has very limited control of what impacts live-cost the most, namely the genetic potential and vitality of the chicks coming to their farm, and the nutritional make-up and quality of the feed. Both arguments are understandable and valid. As the cost of modern poultry barns and utility prices have drastically increased, this argument has reached a fever pitch as the resulting margin for contract growers has decreased significantly (Simpson, Donald, and Campbell, 2007).

The U.S. Department of Agriculture Agricultural Marketing Service (USDA-AMS) has researched this situation and proposed changes for contract broiler growers with the Inclusive Competition and Market Integrity Under the Packers and Stockyards Act (U.S. Federal Register, 2022. The USDA-AMS states,

The proposal would prohibit certain prejudices against market-vulnerable individuals that tend to exclude or disadvantage covered producers in those markets. The proposal would identify retaliatory practices that interfere with lawful communications, assertion of rights, and associational participation, among other protected activities, as unjust discrimination prohibited by the law. The proposal would also identify unlawfully deceptive practices that violate the Packers and Stockyards Act with respect to contract formation, contract performance, contract termination, and contract refusal. The purpose of the rule is to promote inclusive competition and market integrity in the livestock, meats, poultry, and live poultry markets. (U.S. Federal Register, 2022)

The proposal addresses mostly information prior to and during a contract and the business interactions between integrators and contract growers.

Among the changes anticipated from this proposed update to the Packers and Stockyard Act is an end to the traditional tournament pay system to something more “fair,” but the proposal does not lay out exactly what that should be. Instead, one may look to the recent merger between Wayne Farms, Inc. and Sanderson Farms, Inc. to get an idea of the broiler industry’s possible future. Before allowing the merger, in July 2022, the U.S. Department of Justice (DOJ) filed a consent decree offering a settlement of previously filed antitrust suits. According to the DOJ,

The proposed consent decree would:

In response, the newly formed Wayne-Sanderson Farms no longer uses the traditional tournament system of pay for its broiler growers. Their growers receive a base pay rate per pound delivered that does not decrease due to lower performance numbers. Growers’ pay can only increase as an incentive for improved management and the resulting lower live-cost to the company. Still, high live-cost growers may be placed into a probationary “performance improvement program” to help them improve their cost. This probation program is often triggered by such things as poor feed conversion, high mortality, low finish weights, extended time to finish weight, or a combination of these factors. Growers falling into such programs are expected to follow strict management protocols and often receive close oversight in efforts to help improve the farm’s live-cost within a set timeframe of often a year or more. Failing to improve could ultimately result in contract termination. The performance criteria that trigger such programs may yet be tightened as part new contracts, potentially making it tougher for a grower to avoid probation. (It should be noted that most growers who enter these programs do achieve live-cost improvement, exit the programs, and continue to grow for the integrators.)

Growers who have worked under the new Wayne-Sanderson pay system for more than one flock have revealed in private interviews that it has been an overall positive change for them so far. The long-term impact on the growers remains to be seen.

The poultry supply chain is also integrated and impacts along this supply chain have multiplier effects. Because of biological lags in production, a disruption in the supply chain cannot be immediately addressed and can have longer term effects. In recent years, poultry producers have faced tremendous uncertainty with respect to emerging issues such as the COVID-19 pandemic, political disruptions, changing market preferences, and highly pathogenic disease, among others. These disruptions can cause many issues, including processing bottlenecks that affect the timing of grow-out and processing, such as during COVID-19 (Weersink et al., 2021), However there may be demand upside from a consumer preference standpoint, such as the COVID-19 pandemic leading to increased demand at retailers for products to be made at home (Tonsor, Lusk, and Tonsor, 2021). Other production disruptors include energy costs, whose fluctuations can impact growers’ cost of production. We will focus on the most recent supply chain disruption for the rest of this section.

A substantial concern among poultry growers is emerging diseases. Highly Pathogenic Avian Influenza (HPAI) is especially concerning as it has been a large global poultry production disruptor. HPAI is an influenza virus that is easily transmitted between birds and leads to high mortality and morbidity rates. It can be carried bywildfowl populations to domestic birds or through indirect contact (i.e., fomites). Avian influenza was first described in 1878 but emerging highly pathogenic strains have made it a substantial threat to commercial poultry (Lupiani and Reddy, 2009).

In the last decade, two HPAI events have caused substantial impacts on the poultry industry. The 2014/2015 event affected 50.4 million birds in the United States and cost taxpayers nearly $1 billion dollars in control costs (Johansson, Preston, and Seitzinger, 2016; Seeger et al. 2021; Hagerman and Marsh 2016), allowing for responses, biosecurity, and seasonal changes to help eradicate HPAI. Unfortunately, the latest HPAI event did not follow seasonal patterns, carrying on through 2022 into 2023, affecting more than 58 million birds, with 77% of these birds in the commercial egg industry, 17% turkey, 5% broiler, and the rest as backyard or other poultry flocks. The 2022 strand has been shown to be host-adapted—meaning it does not have high mortality rates in wild birds—and older flocks and turkeys have been more susceptible (Elbers et al., 2007; Jerry et al., 2021). Rapid depopulation and control areas are used to try to reduce the viral load from infected premises. Growers may be compensated through indemnity payments for lost birds, but they are responsible for lost income arising from extended periods between flocks as well as associated losses for other normal streams of income like litter sales (Thompson and Hagerman, 2023). A few commercial insurance companies offer umbrella-type policies that could cover these and other losses from HPAI outbreaks, but the policies vary in cost and scope. These losses can be stressful and lead to financial distress (Thompson and Hagerman, 2023). Because of lost bird populations and movement restrictions that impact processing and distribution, increased efforts are being made to support biosecurity to limit the introduction and spread of disease on farms and vigilant monitoring and surveillance efforts. The aim is to minimize supply chain disruptions in production, processing, distribution, consumption, and trade, all of which can have direct or indirect impacts on poultry producers through lost revenue, increased out times, or changes in costs of production.

In the United States, the agriculture industry is governed primarily by the U.S. Department of Agriculture (USDA). Additionally, court decisions and legislative actions all play a large role in how U.S. agriculture works. Recent court cases have had a significant impact, and pending cases could do the same. Potential class action litigation filed in 2022 involving former contract growers argued that growers are employees and not independent contractors. Diaz v. Amick Farms, LLC and Parker v. Perdue Farms, Inc. both focus on claims that the tournament system of grower pay violates the Fair Labor Standards Act (FLSA). Under federal law, employers must pay a minimum wage (federal or state, if the state has set one higher than the federal minimum wage) for hours worked. The former growers argue that, as employees, the poultry companies must pay a minimum wage under the FLSA, and that the tournament system provides less than the required minimum wage. At the same time, litigation argues that growers are entitled to overtime under FLSA for hours worked over 40 hours per week. The issue with this argument is that the FLSA provides an agricultural work exemption from overtime requirements. Currently, a federal judge has denied Perdue’s motion to dismiss the claims, but this is not unexpected in the early stages of litigation. This litigation is just in the initial stages, and it is unclear how it will proceed at this point.

Integrators and contract growers continue to face environmental and right-to-farm litigation. A good example of this is from Oklahoma. In 2005, the state of Oklahoma filed a lawsuit against several poultry companies that had contract growers in the Illinois River watershed in Oklahoma. The claims in the lawsuit that went forward to trial included a "violation of Resource Conservation and Recovery Act (RCRA) 42 U.S.C. § 6972; state law public nuisance and state law nuisance per se; federal common law nuisance; trespass; and two claims under Oklahoma state law” (Richardson, 2023). Before trial, the court dismissed damages and cost recovery claims under the Comprehensive Environmental Response, Compensation and Liability Act (CERCLA), a Solid Waste Disposal Act (SWDA) citizen suit, unjust enrichment, and two claims of violating Oklahoma state law. After the trial, the court dismissed the RCRA claim, state law negligence per se claim, and the two state law claims. The trial lasted from 2009 to 2010, and a delayed decision by the judge in 2023 found that the poultry companies were liable on the merits for the state law nuisance, federal common law nuisance, trespass, and the surviving state law claim. The judge gave Oklahoma and the poultry companies until March 17, 2023, to reach a settlement agreement based on his decision, but that date was recently extended as the parties were in mediation talks with a retired federal judge. Those mediation talks recently failed, and the parties await the federal judge’s decision.

Instance of litigation involving larger animal operations continue to increase. One need only look to North Carolina to see the consistent litigation involving pork companies contracting with growers in the state (Goeringer, 2021). At the same time, individuals and environmental groups with the Environmental Protection Agency recently filed a civil rights complaint claiming that North Carolina’s Environmental Management Commission and Department of Environmental Quality violated the Civil Rights Act of 1964, a federal law, by failing to adequately regulate poultry litter applications in the state (Held, 2023). The legal proceedings are presently in their early phases, and the way forward remains uncertain.

The U.S. poultry industry has overcome many hurdles to arrive at its current position as the producer of top animal protein consumed. The advantages gained from vertical integration have played a primary role in the industry’s ability to meet challenges and overcome volatile markets through rapid adaptation. Supply chains have evolved to fit the model, and must continue to evolve, with the contract poultry grower comprising a key link in the chain. Some of the changes may be the result of legal action or governmental regulation, with or without the consent of all the affected parties. Further changes to the model will be in direct reaction to uncontrollable biological disease challenges. Still other challenges arise from simple economics and price inflation. As the vertical integration model is being challenged on multiple fronts, the industry must find new ways to adapt. Whether it be continued movement toward larger “conglomerate farms,” modified contracts giving growers more revenue but less direct control of their farms, or integrators carrying the bulk of new facility costs, the changes will likely be easier for the poultry companies to navigate, given their adaptability and financial strengths, than for the individual growers, given their already highly leveraged farms. Ultimately, the future of the traditional family poultry farm may well be hanging in the balance.

Diaz v. Amick Farms, LLC. 2022. Complaint, No. 5:22-CV-01246 (D. S.C. April 18, 2022). Available online: https://bit.ly/3PINHqU [Accessed October 6, 2023].

Elbers, A.R.W., J.B. Holtslag, A. Bouma, and G. Koch. 2007. “Within-Flock Mortality during the High-Pathogenicity Avian Influenza (H7N7) Epidemic in the Netherlands in 2003: Implications for an Early Detection System.” Avian Diseases 51(s1):304–308.

Goeringer, P. 2021, May. “Federal Judge Allows New Lawsuit to Continue against Smithfield and Murphy-Brown.” Maryland Risk Management Education Blog. Available online: https://www.agrisk.umd.edu/post/federal-judge-allows-new-lawsuit-to-continue-against-smithfield-and-murphy-brown [Accessed October 5, 2023].

Hagerman, A.D., and T.L. Marsh. 2016. “Theme Overview: Economic Consequences of Highly Pathogenic Avian Influenza.” Choices 31(2).

Held, L. 2023, May 3. “Unchecked Poultry Farming in North Carolina Violates Civil Rights, Residents Say.” Civil Eats. Available online: https://civileats.com/2023/05/03/unchecked-poultry-farming-in-north-carolina-violates-civil-rights-residents-say/ [Accessed October 5, 2023].

Jerry, C., D.E. Stallknecht, C. Leyson, R. Berghaus, B. Jordan, M. Pantin-Jackwood, and M.S. França. 2021. “Age- Associated Changes in Recombinant H5 Highly Pathogenic and Low Pathogenic Avian Influenza Hemagglutinin Tissue Binding in Domestic Poultry Species.” Animals 11(8):2223.

Johansson, R.C., W.P. Preston, and A.H. Seitzinger. 2016. “Government Spending to Control Highly Pathogenic Avian Influenza.” Choices 31(2).

Livestock Marketing Information Center. 2023. “Meat Consumption Annual.” Membership Only Graphs. Available online: https://www.lmic.info/members-only/graphs/meat [Accessed May 11, 2023].

Lupiani, B., and S.M. Reddy. 2009. “The History of Avian Influenza.” Comparative Immunology, Microbiology and Infectious Diseases 32(4):311–323.

National Chicken Council. 2023. “Per Capita Consumption of Poultry and Livestock, 1965 to Forecast 2022.” Available online: https://www.nationalchickencouncil.org/about-the-industry/statistics/per-capita-consumption-of-poultry-and-livestock-1965-to-estimated-2012-in-pounds/ [Accessed October 5, 2023].

Parker v. Perdue Farms, Inc. 2022. Complaint, No. 5:22-CV-00268-TES. (M.D. Ga. July 22, 2022). Available online: https://bit.ly/3Q6wF7t [Accessed October 6, 2023].

Parker v. Perdue Farms, Inc. Order Motion to Dismiss, No. 5:22-CV-00268-TES, WL 17553008 (M.D. Ga. Dec. 9, 2022). Available online: https://bit.ly/48MALsC [Accessed October 10, 2023].

Richardson, J. 2023. “Oklahoma Prevails in Lawsuit Against Poultry Growers for Pollution of Illinois River.” Southern Ag Today 3(7.5). Available online: https://southernagtoday.org/2023/02/oklahoma-prevails-in-lawsuit-against-poultry-growers-for-pollution-of-illinois-river/ [Accessed October 5, 2023].

Seeger, R.M., A.D. Hagerman, K.K. Johnson, D.L. Pendell, and T.L. Marsh. 2021. “When Poultry Take a Sick Leave: Response Costs for the 2014–2015 Highly Pathogenic Avian Influenza Epidemic in the USA.” Food Policy 102(July):102068.

Simpson, G., J. Donald, and J. Campbell. 2007. “Evaluating Cost Trends to Plan Profit-Saving Strategies.” Poultry Engineering, Economics & Management Newsletter (45). Available online: https://ssl.acesag.auburn.edu/poultryventilation/documents/nwsltr-45costtrends.pdf [Accessed October 5, 2023].

Thompson, J.M, and A.D Hagerman. 2023. “Stress and Resiliency among Confined Animal Producers.” Choices 38(1).

Tonsor, G.T., J.L. Lusk, and S.L. Tonsor. 2021. “Meat Demand Monitor during COVID-19.” Animals 11(4):1040.

U.S. Department of Agriculture. 2023a. Quick Stats. Washington, DC: USDA National Agricultural Statistics Service. Available online: https://quickstats.nass.usda.gov/results/9990F2F8-D41F-30FE-9657-54BD76883D45 [Accessed May 11, 2023]

———. 2023b. “Retail Prices for Beef, Pork, Poultry Cuts, Eggs, and Dairy Products.” Washington, DC: USDA Economic Research Service. Available online: https://www.ers.usda.gov/data-products/meat-price-spreads/ [Accessed May 11, 2023].

U.S. Department of Justice. 2022, July 25. “Justice Department Files Lawsuit and Proposed Consent Decrees to End Long-Running Conspiracy to Suppress Worker Pay at Poultry Processing Plants and Address Deceptive Abuses Against Poultry Growers.” Press Release. Washington, DC: USDOJ Office of Public Affairs Press Release. Available online: https://www.justice.gov/opa/pr/justice-department-files-lawsuit-and-proposed-consent-decrees-end-long-running-conspiracy [Accessed October 5, 2023].

U.S. Federal Register. 2022. “Inclusive Competition and Market Integrity Under the Packers and Stockyards Act.” Available Online: https://www.federalregister.gov/documents/2022/10/03/2022-21114/inclusive-competition-and-market-integrity-under-the-packers-and-stockyards-act [Accessed October 5, 2023]

Weersink, A., M. von Massow, N. Bannon, J. Ifft, J. Maples, K. McEwen, M. McKendree, et al. 2021. “COVID-19 and the Agri-Food System in the United States and Canada.” Agricultural Systems 188(March), 103039.