In 2018, U.S. pork buyers filed class action antitrust lawsuits against a group of the largest pork processors in the country. The plaintiffs alleged that these pork processors engaged in an unlawful conspiracy to limit pork production with the purpose of fixing, increasing, and stabilizing wholesale and retail pork prices as early as January 2009 and violated Section 1 of the Sherman Act (1890). This article examines competition (business conduct) issues revealed during the on-going pork antitrust litigation.

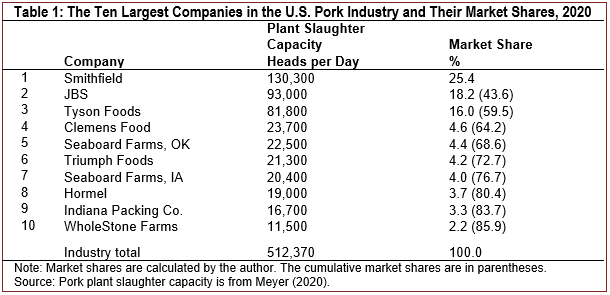

Note: Market shares are calculated by the author. The

cumulative market shares are in parentheses.

Source: Pork plant slaughter capacity is from Meyer

(2020).

The U.S. pork industry is concentrated, meaning that several large pork processors control a large share of pork production and sales in the country (MacDonald, Dong, and Fuglie, 2023). Smithfield Foods, JBS USA, and Tyson Foods are the three largest pork processors, with 2020 hog slaughtering market shares of 25.4%, 18.2%, and 16.0%, respectively (Table 1). They were followed by a group of smaller pork processors with market shares in the range of 2.2%–4.6%. The combined market share of the 10 largest pork processors in 2020 was 85.9% (Table 1).

The U.S. pork industry is vertically coordinated, meaning that hog producers and pork processors use a variety of marketing (forward) contracts to sell/purchase hogs that are alternatives to the negotiated spot (cash) markets. For example, in 2019 the shares of hog purchases that took place in the spot (cash) market and under marketing contracts (swine/pork market formula, other market formula, and other purchase arrangements) were 2% and 62%, respectively (Greene, 2019, Figure 2).

According to marketing contracts, hog producers agree to sell specified quantities of hogs to hog buyers (e.g., pork processors) at a specified future date in exchange for a payment. Marketing contracts establish a price determination method (a price formula) for the hog price to be determined later, when hogs are delivered to the buyer location (a pork processing plant). For example,swine/pork formula contracts use the spot hog and pork prices as base prices to calculate actual hog prices paid to hog producers. Other market formula contracts use futures and options prices as base prices to calculate actual hog prices paid to hog producers (Greene, 2019).

The U.S. pork industry is vertically integrated, meaning that large pork processors control the product (hog/pork) ownership at least at two adjacent stages of the pork supply chain. These pork processors use production contracts to procure hogs and/or own and operate hog farms. The share of hogs raised under production contracts was 69% in 2015 (Davis et al., 2022: Table 5).

Pork processors own hogs produced under production contracts, according to which hog producers raise (feed and finish) pigs/hogs for pork processors in exchange for a fee (Davis et al., 2022). Consequently, pork processors make production, marketing, and pricing decisions, including decisions on hog quantities produced by hog producers under these contracts.

Typically, under production contracts pork processors are responsible for providing pigs, feed, veterinary and medical supplies and services, transporting pigs to and from the farms, and determining production management practices (Davis et al., 2022; Bolotova 2022). Hog producers are responsible for providing hog housing facilities, land, labor, utilities, and operating expenses and following production management practices determined by pork processors.

A dramatic increase in feed prices, coupled with the effect of hog production and price developments, adversely affected the profitability of pork processors beginning in 2009 (Giamalva, 2014). The prices of corn and soybean meal, the two major feed types used in hog production, started increasing dramatically in 2008 (Becker, 2008). Pork processors, who used production contracts with hog producers and/or owned hog farms,had to pay higher feed prices. Feed costs account formore than 65% of all pork production expenses (Pork Checkoff, 2009-2011). Pork processors, who purchased their hogs using the spot market and/or marketing contracts, had to pay higher hog prices, which were due to higher feed prices.

The largest pork processors implemented production cuts at various stages of the pork supply chain beginning in 2009. These production cuts were necessary to decrease quantities of hogs and pork produced in the period of increasing feed prices and weakening demand to maintain a viable profitability level and to avoid financial losses (Giamalva, 2014).

The largest pork processors periodically made public statements regarding the industry oversupply problem adversely affecting their profitability and their intent to implement production cuts. The following excerpts are two examples:

In 2018, a group of pork buyers filed class action antitrust lawsuits against the largest pork processors in the country, alleging that they had engaged in an unlawful pork price-fixing conspiracy as early as January 2009. In their complaints, the pork buyers stated that the largest pork processors implemented the following allegedly anticompetitive and coordinated production cuts to decrease quantities of hogs and pork produced to increase wholesale and retail pork prices (In Re: PAL, 2020, 2022). The combined market share of the largest pork processors, who implemented production cuts, was approximately 80%.

The pork buyers (plaintiffs) alleged that the largest pork processors engaged in a pork price-fixing conspiracy (cartel) by publicly communicating their intentions to implement production cuts and by sharing private, competitor-sensitive information related to production, costs, and profit (In Re: PAL, 2020, 2022). The information exchanges were accomplished by partnering with Agri Stats, a third-party data aggregation service.

The plaintiffs claimed that the alleged pork price-fixing cartel was a violation of Section 1 of the Sherman Act (1890). As a result, they had to pay higher prices forpork products and were overcharged. Section 1 of the Sherman Act prohibits contracts, combinations, and conspiracies in restraint of trade in interstate commerce. Price-fixing agreements (cartels or conspiracies) are examples of the restraints of trade that are most damaging to the market. Price-fixing agreements aim to increase, decrease, or fix (stabilize) product prices and can be verbal, written, or inferred from the conduct of firms (Federal Trade Commission, 2024).

The market effects of a typical output price-fixing cartel are a decrease in the product quantity available in the market, an increase in the product price buyers have to pay, a welfare transfer from buyers to producers (overcharge), and a deadweight loss, due to which there are buyers who do not purchase the product because of higher prices. The overcharge is the basis for damages that plaintiffs aim to recover during antitrust litigations.

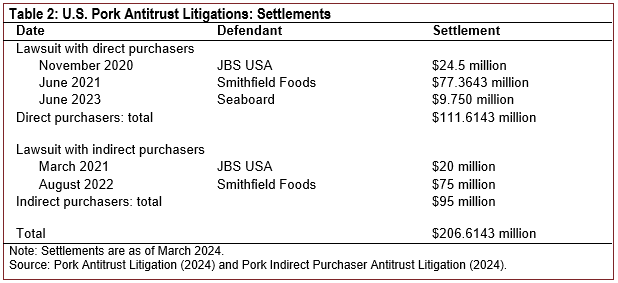

Note: Settlements are as of March 2024.

Source: Pork Antitrust Litigation (2024) and Pork Indirect

Purchaser Antitrust Litigation (2024).

The overcharge measured in dollars per pound of pork is the difference between the pork price during the alleged cartel period and the pork price during a more competitive period (e.g., during the pre-cartel period). The total dollar overcharge attributed to all pork buyers is the overcharge measured in dollars per pound times pork quantity sold during the alleged cartel period. Overcharges are calculated using transaction prices obtained from the defendants.

The buyers who purchased pork products directly from the pork processors (e.g., food retailers and wholesalers) are entitled to recover treble damages (3 times the overcharge) under the Clayton Act (1914). The buyers who purchased pork products indirectly from the pork processors (e.g., final consumers) are entitled to recover damages in selected states, where antitrust laws allowing indirect buyers to recover damages due to antitrust violations exist.

Table 2 summarizes settlements reached by some pork processors as of March 2024. The total settlements reached by Smithfield Foods, JBS USA, and Seaboard with direct and indirect purchasers are $206.6143 million. In their settlement agreements, these pork processors do not admit to any wrongdoing.

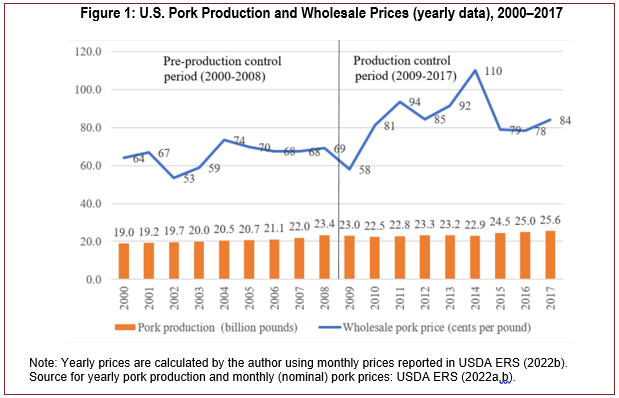

Figure 1 depicts yearly pork production and wholesale pork prices for the pre-production control (Pre-PC) period (2000–2008) and the production control (PC) period (2009–2017). Total pork production each year is affected by the number of hogs slaughtered and the weight of each hog. An analysis of yearly changes in pork production indicates that there was a consistent increase in pork production in the pre-PC period, which might have reflected the pork oversupply problem. In the PC period, decreases in pork production in selected years were observed. These ranged from -0.27% in 2013 to -2.45% in 2010.

The following changes in the pork industry dynamics in the PC period, as compared with the pre-PC period, are reported in the literature (Bolotova, 2022). The yearly average pork production increased by 15% (20,600 million to 23,628 million pounds). While the implementation of production cuts on average did not decrease pork quantities produced in the PC period, it might have decreased the pork production’s growth rate. The yearly average pork export increased by 105.6% (2,424 million to 4,983 million pounds). A substantial increase in pork export decreased pork quantities available for domestic consumption in the PC period. The yearly average pork quantity available for domestic consumption increased by 2% (19,013 million to 19,370 million pounds). The yearly average pork quantity available per capita decreased by 6.2% (65 to 61 pounds).

A decrease in the product quantity available for domestic consumption would generally increase this product’s price. The monthly average wholesale pork price increased by 29% in the PC period ($0.66 to $0.85 per pound). This pork price increase is likely to reflect increases in feed (corn and soybean meal) costs. The monthly average farm-to-wholesale margin increased by 8% (32.5% to 35.1% of the wholesale pork price). The farm-to-wholesale margin includes pork processing costs and profit of pork processors. The observed increase in the farm-to-wholesale margin might reflect increasing pork processing costs and/or increasing profit of pork processors in the PC period. The latter may be due to a short-term increase in their seller market power achieved due to production cuts.

The analysis of competition problems revealed during the on-going pork antitrust litigation suggests the following implications for business and policy decision-making.

In their settlement agreements, the pork processors do not admit to any wrongdoing. The economic rationale for implementing production cuts exists. According to microeconomic theory, if the industry faces increased costs, the industry will decrease output quantity to pass

the cost increase on the buyers of their output in theform of higher output prices (Bolotova, 2022). Pork processors who owned hog farms and/or used production contracts had to pay higher feed pricesbeginning in 2008. To pass the feed cost increase on pork buyers, pork processors had to decrease hogquantities and, consequently, pork quantities produced. Had not pork processors implemented production cuts, they would have overproduced (oversupplied) hogs and pork, received pork prices below production costs, and incurred financial losses. The latter would have further worsened the hog/pork oversupply problem the pork industry already faced by 2008 (Giamalva, 2014).

The pork buyers alleged that the pork processors partnered with Agri Stats, a third-party data aggregation service, to enforce their cartel agreement by being able to monitor each other’s production and pricing and to discipline cartel members for not complying with their agreement (In Re: PAL, 2020). Agri Stats collected confidential production and financial data from pork processors, then processed and shared these data back with pork processors.

The U.S. Federal Trade Commission informs that sharing information on output, costs, prices, customers, or strategic planning may represent competition concerns (Bloom, 2014). In September 2023, the U.S. Department of Justice (DOJ) filed a civil antitrust lawsuit against Agri Stats alleging that its data-sharing service provided to pork, broiler chicken, and turkey processors was a violation of Section 1 of the Sherman Act (U.S. Department of Justice v. Agri Stats, 2023). The largest pork, broiler chicken, and turkey processors are named as co-conspirators in the complaint. The DOJ requests the court to rule that Agri Stats’s and its broiler, pork and turkey co-conspirators’ anticompetitive information exchanges have unreasonably restrained trade and are unlawful under Section 1 of the Sherman Act. In addition, the DOJ requests the court to permanently enjoin Agri Stats from facilitating exchanges of sensitive information and from continuing engaging in the anticompetitive practices described in the complaint.

The concerns about a high level of concentration in the pork industry and the ability of the largest pork processors to exercise seller market power potentially leading to higher pork prices are likely to remain in the future. For the market concentration to decrease, new firms have to enter pork processing. In March 2023, U.S. Department of Agriculture announced that $89 million would be allocated to finance the startup and expansion of independent meat processors as part of the Biden-–Harris Action Plan for a Fairer, More Competitive, and More Resilient Meat and Poultry Supply Chain (U.S. Department of Agriculture, 2023). Hog producers should consider entering pork processing. These producers may benefit from organizing their pork processing businesses as the Capper–Volstead Cooperatives, which collective marketing activities have a limited antitrust immunity to the Sherman Act.

The modern hog market is characterized as thin because the share of hogs sold in the spot market is small relative to the share of hogs sold using marketing contracts and the share of hogs procured under production contracts (Adjemian et al., 2016). To some extent, thin markets lack market and price transparency, and they may be prone to market and price manipulation. Considering high market concentration in the pork industry, an increasing use of production contracts by pork processors may raise competition issues related to their buyer market power in the near future, possibly leading to lower prices for hog producers (McVan, 2022). Similar buyer market power issues have been raised in the broiler chicken industry, where 90% of broiler chickens are produced under production contracts between broiler chicken growers and broiler chicken processors (Shaffer, 2017).

To inform future policy directions and provide information relevant to market monitoring efforts, the following research directions are suggested: The first is to evaluate changes in the structure and performance of the U.S. pork industry over time to understand the effects of the industry shift to production contracts and the entry of new pork processing businesses organized by hog producers. The second is to evaluate the structure of production contracts, design of payment systems included in these contracts, and factors affecting hog producers’ preferences for production contracts. Finally, research relevant for hog producers planning to enter pork processing would evaluate alternative legal forms of doing business that would be most beneficial for them.

Adjemian, M.K., B.W. Brorsen, W. Hahn, T.L. Saitone, and R. J. Sexton. 2016. Thinning Markets in U.S. Agriculture What are the Implications for Producers and Processors? USDA Economic Research Service, Economic Information Bulletin 148.

Becker, G.S. 2008. Livestock Feed Costs: Concerns and Options. Congressional Research Service, Report for Congress RS22908.

Bloom, M. 2014. Information Exchange: Be Reasonable. Federal Trade Commission, Bureau of Competition. Available online: https://www.ftc.gov/enforcement/competition-matters/2014/12/information-exchange-be-reasonable

Bolotova, Y. 2022. “Price-Fixing in the U.S. Broiler Chicken and Pork Industries.” Applied Economics Teaching Resources 4(4):55–91.

Davis, C.G., C. Dimitri, R. Nehring, L.A. Collins, M. Haley, K. Ha, and J. Gillespie. 2022. U.S. Hog Production: Rising Output and Changing Trends in Productivity Growth. USDA Economic Research Service, Economic Research Report 308.

Federal Trade Commission. 2024. Price Fixing. Available online: https://www.ftc.gov/tips-advice/competition-guidance/guide-antitrust-laws/dealings-competitors/price-fixing

Giamalva, J. 2014. Pork and Swine: Industry & Trade Summary. U.S. International Trade Commission, Office of Industries Publication ITS-11.

Greene, J.L. 2019. Livestock Mandatory Reporting Act: Overview for Reauthorization in the 116th Congress. Congressional Research Service, Report R45777.

In Re: Pork Antitrust Litigation. 2020. Case 0:18-cv-01776-JRT-HB. Direct Purchaser Plaintiffs’ Third Amended and Consolidated Class Action Complaint filed on 01/15/20. Available online: https://porkantitrustlitigation.com/assets/documents/2020-01-15-DPP Third Amended complaint.pdf

———. 2022. Civil No. 18-cv-1776 (JRT/HB). Consumer Indirect Purchaser Plaintiffs’ Fourth Amended Consolidated Class Action Complaint filed on 01/12/22. Available online: https://www.overchargedforpork.com/assets/Docs/Redacted Fourth Amended CIPP Complaint.pdf

MacDonald, J.M., X. Dong, and K.O. Fuglie. 2023. Concentration and Competition in U.S. Agribusiness. USDA Economic Research Service, Economic Information Bulletin 256.

McVan, M. 2022. “Scaling Up: Use of Production Contracts Has Become the Norm.” Investigate Midwest. Available online: https://investigatemidwest.org/2022/09/21/scaling-up-use-of-production-contracts-has-become-the-norm/

Meyer, S. 2020. “Pork Packing: Just What Is Capacity?” National Hog Farmer. Available online: https://www.nationalhogfarmer.com/business/pork-packing-just-what-capacity

Pork Antitrust Litigation. 2024. Available online: https://porkantitrustlitigation.com/

Pork Checkoff. 2009–2011. “The Pork Industry at a Glance: Quick Facts.” Available online: https://porkgateway.org/wp-content/uploads/2015/07/quick-facts-book1.pdf

Pork Indirect Purchaser Antitrust Litigation. 2024. Available online: https://www.overchargedforpork.com/

Shaffer, E. 2017. “Poultry Processors Face Lawsuit Over Grower Pay.” MEAT+POULTRY. Available online: https://www.meatpoultry.com/articles/15785-poultry-processors-face-lawsuit-over-grower-pay

U.S. Department of Agriculture. 2023. Biden-Harris Administration Announces Actions, Investments to Create Fairer Markets, Lower Prices. Press Release No. 0049.23.

U.S. Department of Agriculture Economic Research Service (USDA ERS). 2022a. Food Availability (Per Capita) Data System. Available online: https://www.ers.usda.gov/data-products/food-availability-per-capita-data-system/food- availability-per-capita-data-system/ - Food Availability

———. 2022b. Livestock and Meat Domestic Data. Available online: https://www.ers.usda.gov/ data-products/livestock-meat-domestic-data/livestock-meat-domestic-data

U.S. Department of Justice v. Agri Stats. 2023. Complaint filed on 09/28/23. Available online: https://www.justice.gov/opa/file/1316576/dl?inline