The U.S. fresh fruit and vegetable—produce—industry is very diverse, including over 300 products, each with its own structure at the production and first-handler marketing levels. Despite this diversity, virtually all fresh produce shares two fundamental attributes: perishability and seasonality. The high level of risk observed in the fresh produce sector arises from the combination of product perishability and weather variability. Weather factors can always undo the best-laid plans by unexpectedly shifting short-run supply or demand. Perishability limits storability and the ability of firms to adjust to short-run disequilibria in supply and demand, other than through price, making markets volatile.

This article analyzes the U.S. fresh produce industry based on Michael Porter’s Five Forces model plus two additional forces, as described in Choices by Olson and Boehlje (2010). It is one of a series of articles—published by various authors in Choices in 2010 and 2011—which utilize this expanded forces model to frame the discussion of forces for change in various commodity sectors and industries. The forces include: (1) rivalry among existing competitors, (2) threat of new entrants, (3) bargaining power of suppliers, (4) bargaining power of buyers, and (5) the threat of substitute products (Porter, 2008). The two additional forces affecting competition are: (6) technology and (7) other drivers of change. Please see Olson and Boehlje for an explanation of the combined methodology.

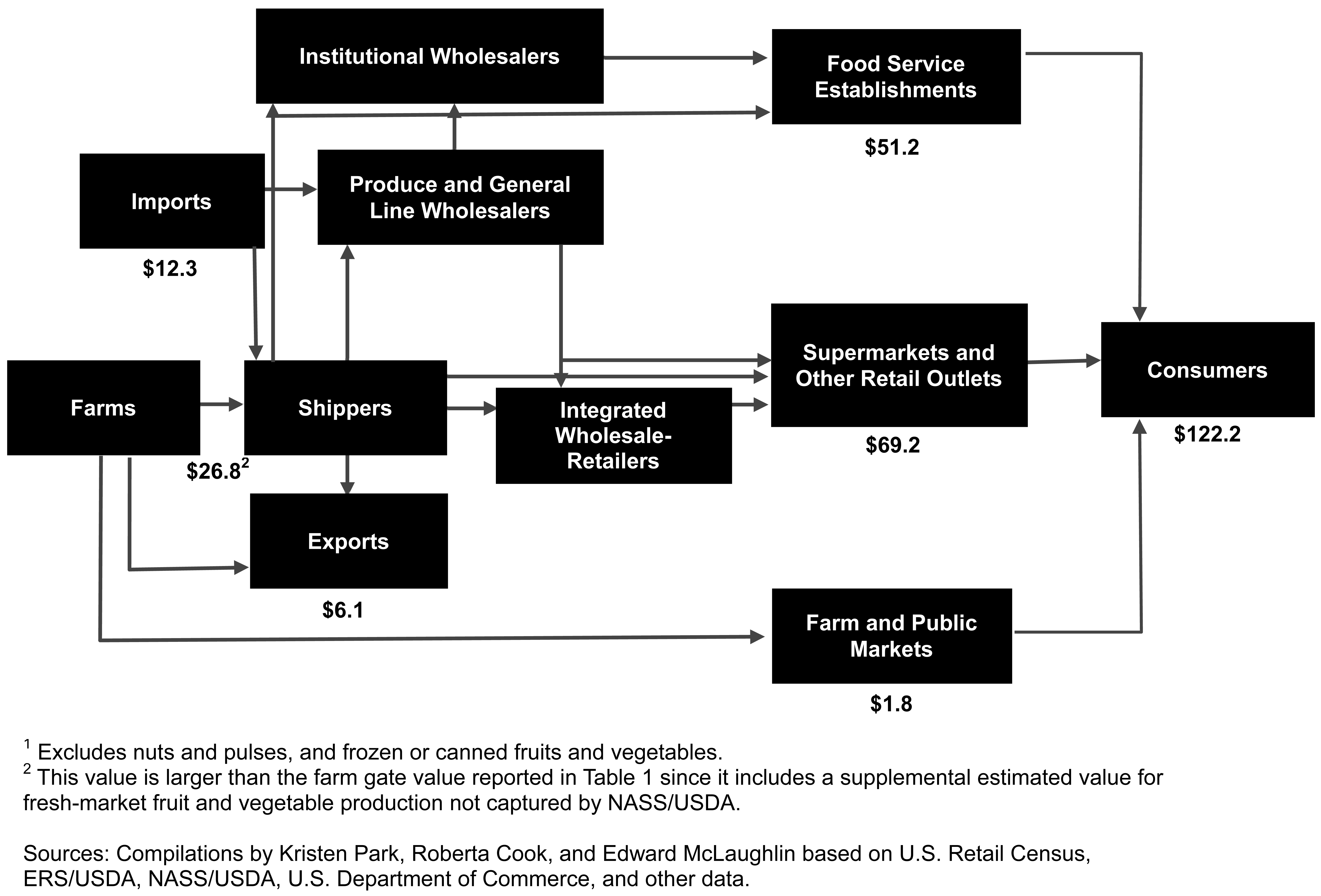

In the United States, the final value of fresh produce sold through all marketing channels was estimated at over $122.1 billion in 2010 (see Figure 1). While the value of produce sold through foodservice channels has been growing, the retail channel still predominates with approximately 57% of sales as compared with 42% for foodservice; the expanding direct-to-consumer channel is estimated to account for less than 2% of total sales. There are many channels through which produce can be marketed, as evident in Figure 1, but the trend has been toward the use of more direct channels with fewer intermediaries, as discussed later.

There were 3.2 million acres of fresh fruits and vegetables harvested in 2010, producing 99.9 billion pounds with a farm gate value of $21.8 billion (see Table 1). Consumption of fresh fruits and vegetables was 313 pounds per capita in 2010, up 27% since 1976, due to growing awareness of the health benefits of fresh produce and greater year-round availability from rising imports.

Fresh produce imports reached $12.3 billion in 2010, almost quadrupling since 1994 in response to growth in consumer demand and the inability to produce many fresh fruits and vegetables year-round in the United States. Exports doubled over the same period, reaching $6.1 billion in 2010; the fresh produce trade deficit grew to $6.2 billion [Foreign Agricultural Service (FAS) of USDA]. According to the Economic Research Service (ERS) of USDA, in 2010 the import share of consumption was 24.1% for fresh vegetables and melons and 31.9% for fruit, excluding bananas (USDA/ERS, 2011a and 2011b).

| Product | Area Harvested | Production | Value | Per Capita Consumption |

|---|---|---|---|---|

| (Acres) | (Million Pounds) | (Million Dollars) | (Pounds) | |

| Fresh vegetables | 1,567,352 | 39,474.10 | 11,316 | 149.2 |

| Fresh potatos | 281,316 | 11,121.30 | 977 | 35.6 |

| Total Fresh Vegetables | 1,848,668 | 50,595.40 | 12,293 | 184.8 |

| Fresh citrus | 281,349 | 7,440.00 | 1,668 | 21.5 |

| Fresh noncitrus | 851,581 | 35,550.80 | 6,994 | 80.8 |

| Melons | 22,030 | 6,319.50 | 856 | 26.1 |

| Total Fresh Fruit | 1,354,960 | 49,310.30 | 9,518 | 128.4 |

| Total Fresh Fruits and Vegetables | 3,203,628 | 99,905.70 | $21,811 | 313.2 |

Market integration in the NAFTA region has increased. Canada is the leading U.S. fresh produce export market, followed by Mexico. Most fresh vegetables are traded intra-NAFTA with Mexico usually supplying about two-thirds of U.S. imports, while fresh fruit trade involves more diverse sources and export markets. Most fresh produce international trade is driven by seasonal production deficits rather than lower prices for imports; proximity to market is key not only due to perishability but transportation costs, so the advantage of any country generally lies with its in-season domestic production.

In the fresh produce industry many types of suppliers service retail and foodservice buyers, including shippers, importers, wholesalers, distributors and brokers. Mounting pressure to streamline the supply chain and drive out nonvalue-adding costs has increased the relative importance of shippers based in key production regions. Shippers are first-handlers essentially acting as marketing agents for growers. In recent decades larger shippers have transitioned from seasonal to year-round operations, sourcing from shifting production regions which follow climatically-determined seasonal patterns throughout the year. This means that many shippers market, and may invest in, production from several states and often other countries.

Shipper headquarters are fixed in their dominant production region, and most are actually grower-shippers—large forward-integrated growers handling and marketing production for themselves as well as other growers. In this way, they assemble a greater supply volume and come closer to matching the scale of the fewer, larger buyers that exist today, allowing growers of all sizes to gain access to major domestic and export markets. These relatively specialized, usually family-controlled grower-shippers control a sizable portion of fresh produce sales at the first-handler level.

The majority of growers and shippers are based in California and Florida except in the case of apples, pears and cherries where firms in the state of Washington predominate. Online queries of a fresh produce industry credit reporting service, The Blue Book, showed that in 2011 there were 3214 total shippers in the United States, including 1259 in California and 465 in Florida (an approximation due to potential classifications of firms in multiple categories).

In 2010, California produced 49% of the value of fresh vegetables grown in the United States, followed by Florida with 14% and Arizona with 8% [National Agricultural Statistics Service (NASS) of USDA]. Most of Arizona’s volume of both fruits and vegetables is marketed by California shippers who have relationships with Arizona growers. In 2009, California produced 53% of the value of U.S. fresh fruit, followed by Washington and Florida with 21% and 8%, respectively (USDA/ERS estimates).

California’s dominance lies in its ability to produce a great diversity of products over extended seasons, whereas other states are confined by climate to either more limited offerings and/or shorter seasons. This article emphasizes trends among California, Florida, Arizona and northwest shippers and their relationships with buyers, since their combined volume represents the vast majority of fresh produce grown in the United States, as well as much of the volume of imports.

In meeting retail and foodservice demand for year-round availability—importing during the off-season when necessary—shippers reduce procurement transaction costs for buyers. Buyer transaction costs are also reduced by the growing role of shippers as gatekeepers for their customers. Shippers apply their considerable expertise and technology to standardize product quality, employ Good Agricultural Practices (GAPs) and traceability mechanisms, and now increasingly social and environmental responsibility best practices; all of which must be achieved across each of a shipper’s growers and production locations, whether in the United States or abroad.

Many standards are market—rather than government—determined and, in either case, are verified by independent third party certifiers, with offices both in the United States and in key foreign export-oriented production locations. Verification systems are designed to minimize but do not eliminate food safety risk. Both GAPs and verification methodologies are evolving rapidly in tandem with knowledge of effective risk mitigation strategies, as well as rising expectations about acceptable risk. Social and environmental responsibility best practices and requirements are still in their infancy but there is a growing understanding that sustainability must be considered on a supply chain-wide basis. Labor practices are receiving growing attention within the emerging social responsibility standards.

Fresh produce industry-wide generalizations are difficult, since structure and the forces driving competition tend to vary by product or groups of products which are usually grown in similar locations and marketed by the same pool of firms—comprising industry subsectors. An example is the apple, pear and cherry subsector. Industry dynamics tend to be quite different for perennial and annual crops due to the variation in production, investment and supply time horizons. For example, even within the berry subsector there are important distinctions between strawberries and bush berries since the latter are perennial crops whereas strawberries are annual. A companion article in this issue compares the lettuce/leafy green and berry subsectors in order to provide more detail on the intricacies of the fresh produce industry.

Perishability is the most important factor influencing firm rivalry in fresh produce.Traditionally fresh produce was also largely an undifferentiated, commodity business. The main dimension of competition has revolved around price rather than product features, services or consumer brand images. Poaching business through lower prices transfers profits downstream and keeps profits relatively low at the production level. The industry is changing as firms respond to expanding consumer demand for convenience and attempt to avoid “the commodity trap” with the introduction of more consumer-friendly packaging, such as produce in clamshells, and other value-added products, as well as new products. Value-added products range from unwashed romaine hearts and artisan lettuce packs to washed, ready-to-eat (RTE) produce referred to as fresh-cut fruits and vegetables, led by bagged salads. However, even with product differentiation, perishability makes price competition hard to avoid.

Exit barriers contribute to more intense firm rivalry. They are relatively high at the fresh produce production and first-handler levels, in many cases due at least as much to owners’ devotion to the business as to highly specialized assets. The family-owned characteristic of many firms contributes to these barriers, as well as to clashes of ego and personality that may have intensified firm rivalry in some subsectors. All of these factors have often kept firms in the market even though they may be earning low or negative returns, contributing to excess capacity and lower profitability for healthy competitors. Periodic weather events that create high-price markets can temporarily breathe life back into weak competitors.

Historically, the high level of production risk and price volatility common to fresh produce commodity markets contributed to a heavy reliance on daily, spot market sales, as opposed to forward contracting between shippers and buyers—the fresh-cut sector is an exception. However, this began to change twenty years ago with the entrance of Walmart with its supercenter format and focus on seasonal and annual contracts with key preferred providers. Higher retail concentration levels since the end of the 1990s have contributed to less reliance on spot markets. Not only are large retailers at risk of insufficient supply if overly reliant on the spot market, but they face greater exposure to food safety risk and less ability to plan and develop effective merchandising and promotional programs in collaboration with suppliers. Hence, the market is gradually moving away from daily prices as the principal dimension of competition, with important implications for firm rivalry and competitive strategies.

Higher concentration levels in both retail and foodservice channels have encouraged consolidation on the supply side. This has generally taken place through merging the marketing operations of shippers into combined larger entities, although acquisition of the production, packing or fresh-cut operations of competitors has also occurred. Larger sales volumes have not only enabled shippers to service bigger accounts, but to invest in more sophisticated marketing, logistical, and other services.

Firms seek out production areas with micro-climates in order to lower production risk, in particular during weeks when production regions shift and supply is less predictable—the shoulder seasons. Larger grower-shippers have greater capacity to invest in the development of new varieties and cultural and postharvest practices designed to improve the consistency of volume and quality in both existing and new production locations.

These strategies are highly valued by buyers and have become important differentiators for suppliers when competing for large accounts. The importance of size as a competitive differentiator is causing more specialization between buyer and seller types.

For example, the competitive wherewithal of some mid-tier firms, such as grower-shippers with $50-125 million in sales, has likely eroded with the largest retailers. Many are finding it more difficult to be the preferred suppliers of large retailers. Losing preferred supplier status means that their sales to this type of buyer may be less consistent, causing them to shift their marketing strategies toward regional retailers, and wholesalers servicing independent retailers, regional foodservice chains and independent restaurant operators. Exceptions are for specialty produce, including exotic, organic or highly seasonal products where there is less uniformity or less of a commodity orientation and where smaller volumes are acceptable. In these cases, mid-tier and smaller suppliers may face less competition when pursuing large accounts.

Today, rather than competing mainly for daily sales, innovative firms seek to become preferred suppliers of key retail accounts and then focus on understanding the needs of that retailer and developing an account-specific marketing program covering multiple seasons. These programs often include specific packs, product sizes and grades, merchandising support, promotional programs—which increasingly incorporate social media, and in some instances logistical support services. While still new, it is becoming more common for these programs to include category development, a costly service. This process involves analyzing the product mix, space allocations and pricing for a category, such as fresh tomatoes, using retailer point-of-sale, scanner data. In this way a retailer’s performance can be benchmarked relative to competitors and opportunity gaps for improving performance identified.

Category analysis has long been the consumer packaged goods (CPG) model, but in the fresh produce department it only existed in the fresh-cut category where products are marketed as CPGs. It was not present in commodity produce for several reasons. Consumer recognized brands, while growing, still play a relatively limited role in fresh produce where shipper trade labels—recognized by commercial buyers rather than consumers—predominate. Seasonality and insufficient volume precluded a particular shipper’s product from being in any given retailer’s stores on a consistent basis. Most produce is sold in bulk on a random-weight basis versus with scannable UPC bar codes, and until widespread adoption of produce price-lookup codes (PLUs), much less data was available. In addition, in the past the high cost of purchasing scanner data was a formidable barrier for most suppliers. Today’s larger suppliers are overcoming many of these barriers, including enough distribution capacity to consistently service a large number of stores.

Today’s fewer, larger buyers increasingly see the benefits of commodity shippers coming closer to the CPG model of providing marketing and promotional support, despite the challenges posed by perishability and weather variability. This awareness is causing more retailers to begin to share their consumer loyalty card data with preferred produce suppliers, as they do with CPG suppliers. Suppliers recognize the opportunities for differentiation relative to competitors as they battle for market share, in particular when competing for steady business from the largest retailers.

The theory is that if suppliers can assist retailers to better target the right consumers in the right stores for the right product with the right price at the right time, both retailers and suppliers will benefit, each becoming more competitive in their respective markets. The development of the marketing capacity to offer these services takes capital, information technology, analytical capacity, retailer cooperation and at least a medium-term time horizon. Mutual commitment must be strong for the investment to be worthwhile. Necessary conditions are for the retailer to commit to sharing data and to consistently sourcing predictable volume from a supplier such that the supplier’s product has assured shelf-space—which has often been lacking. Where suppliers are grower-shippers tied to land bases, it requires them to become more marketing- versus production-oriented firms.

For example, if category analysis shows expanding consumer demand for certain varieties of apples relative to others, or demand in seasons for which they have insufficient supply, grower-shippers may need to adjust their production bases; and firms do indeed report responding to these types of market signals. A new entrant to fresh produce distribution, C.H. Robinson, a logistical services company, became successful as a national distributor without backward-integration into production, in large part due to its investment in category development services for its buyers, and ability to source wherever necessary. This set an important new benchmark for all suppliers.

More commodity shippers are also conducting consumer research as part of their enhanced marketing and promotional support services, better enabling retailers to target the right customers, thereby increasing sales for both shipper and retailer. In general, marketing services are a rapidly emerging dimension of competition. Intense firm rivalry at both the supplier and retailer levels generates strong incentives for closer cooperation for both buyers and sellers.

Despite the growing efforts of suppliers to differentiate themselves, with perishability always a given, firms still largely operate in a commodity business. Shippers whose offerings include the product of affiliated growers—the majority—are always mindful of the net returns they pay to growers. Grower relationships with shippers are mainly based on marketing agreements rather than price contracts, and these agreements are often short-term. The net return to the grower is the residual of the market price for his product minus pick, pack, haul to shed, cooling, palletization, marketing and other shipper charges. Shippers control these functions in order to standardize their offerings across growers, supporting a consistent trade label or brand.

Most of these charges are to carry out immediate physical functions whereas the purpose of marketing charges may seem more nebulous to growers. Growers may view charges for special promotions or other marketing services as merely cents off the net return/box rather than as investments stimulating enhanced shipper-buyer relationships and pricing over the longer run. There is a horizon problem, and growers dissatisfied with short-term net returns are prone to change handlers accordingly, attempting to maximize current returns rather than investing in potentially higher future returns. Thus, suppliers engaging in the customer/consumer marketing arena are proceeding with caution, recognizing that investment in differentiation strategies is constrained by the competitive realities of commodity markets.

While the dimensions of competition have expanded and in doing so somewhat reduced the relative importance of price, in absolute terms price is as important as ever, driven by the economic downturn. Intense firm rivalry continues unabated at the retail level. Many more types of retailers and store formats now sell groceries—supercenters, club stores, dollar stores, limited assortment stores, drug stores—contributing to a phenomenon known as channel blurring. While this trend had been unfolding over the last twenty years, it intensified during the recession and operators of all types of store formats have been challenged to compete more on price, including the heavy price discounters. In 2009, many retailers experienced negative same store sales growth and by this metric some, including Walmart and Supervalu, had still not turned the corner as of mid-2011.

The same trend has occurred in foodservice channels where many chains are struggling to rebound from the recession and where virtually all operators have had to introduce lower price options into their menus to address the consumer trend of trading down when eating out. Retail and foodservice margin pressure has been transferred upstream in the supply chain just as suppliers were attempting to become more marketing- and service-driven. The above trends have driven firms at all levels of the supply chain to seek efficiency gains, including through the application of information technology, to achieve better resource management, discussed later.

The recession also stimulated retail demand for private labels/retailer store brands, a relatively new phenomenon in the fresh produce department outside of the fresh-cut category. Private label fresh produce supermarket sales surpassed $3.1 billion in 2010 (Food Institute Report, 2011). Demand for private labels is now particularly strong for fresh-cut produce and becoming somewhat of a factor for some commodities—citrus, potatoes, apples, mushrooms, lettuce, tomatoes—with important implications for suppliers.

Private labels might be seen by suppliers as a double-edged sword. While they assure dedicated shelf-space and may be a differentiator for suppliers willing to provide them, prices for the supplier are often lower while the costs of packing multiple labels are higher. In comparison with CPG products, marketing expenditures are low. Hence, elimination of supplier marketing expenditures for fresh produce private labels yields few savings to offset lower prices. Furthermore, fresh produce production is generally a low margin business compared with manufacturing of CPG products.

Many produce firms are currently determining whether and where private labels fit into their strategic positioning in the marketplace, especially those firms recently investing in promoting their trade labels all the way to the consumer. Nevertheless, growth in the relative bargaining power of buyers means that more suppliers may need to consider offering private labels as part of the toolkit they use in competing with rival suppliers.

Today, twenty buyers are estimated to control approximately two-thirds of the value of groceries sold nationally. In 2010, there was a total of 138 retail chains—10 or more stores—operating in the United States, including 40 chains with over 100 stores each (Nielsen/Progressive Grocer, 2010). These increasingly powerful buyers can capture more value by exerting downward pressure on prices, and demanding better quality and services, all of which is the behavior discussed earlier.

Independent of market structure, product perishability has always tended to limit the bargaining power of produce suppliers relative to buyers, as expressed by the industry adage “sell it or smell it.” It is not uncommon for produce to be sold at the first-handler level at a price covering only variable—pick, pack, packaging, and marketing—costs, with no return to the farm for weeks at a time.

In the produce industry, relative bargaining power varies in the short-term, depending on weekly supply and demand. For example, weather events can shift iceberg lettuce prices from $10/box one week to $30 the next. When markets are short, shippers pro-rate their forward commitments and the volumes sent to different customers depends in part on the loyalty of a customer to the shipper under normal market conditions. The negotiating tables are turned. Markets are more often long than short, so many sellers exercise caution when they have the upper hand, although others seek to maximize short-term profits.

The growth of forward contracting has made it more challenging for shippers to manage through periods of short supply and cover contracts, and reduced their relative bargaining power during these periods when high profits on the spot market typically offset spot market losses during periods of long supply. On the other hand, shippers may achieve better than average spot market prices during other periods. Both buyers and sellers continually evaluate the pros and cons of contracts, and relative bargaining power influences the negotiated prices and adjustment mechanisms when spot market prices differ greatly from the former.

In contrast to most food manufacturers, fresh produce suppliers are generally not large enough to service the total demand of national chains. Only Dole, Chiquita and Del Monte can fully supply today’s multi-billion dollar retailers and, with the exception of Dole, that is mainly for bananas. Chains have multiple banners and numerous distribution centers (DCs) and produce suppliers compete to service specific DCs and/or retail chain divisions. The greater the supplier’s product availability—seasons and volume, quality, services and overall competitiveness, the greater their bargaining power and the more DCs they may be selected to service. When firms become preferred suppliers and develop more of a partnership or collaborative relationship, their value increases.

Interestingly, the enormous volume requirements of buyers and the relative size difference with suppliers somewhat mitigates buyer bargaining power in the sense that obtaining week-in, week-out supply can be challenging. Retailers typically see the fresh produce department as a key point of differentiation relative to competitors and, on average, it generates roughly 10% to 12% of the sales of conventional supermarkets; this makes it vital to have fully stocked shelves. The magnitude of the volume requirements of large retailers is highlighted by the following examples (Planet Retail online queries, 2011). Sales of fresh produce in 2010 through Walmart’s principal—and non-traditional grocery—format, the supercenter, are estimated at $9.7 billion. Kroger, the second largest grocery retailer and the largest traditional food retailer, is estimated to have sold $8 billion of fresh produce in 2010. The club store format has also become a very significant outlet for fresh produce, with Costco’s fresh produce sales estimated at $2.7 billion.

More attention is being placed on varieties as an emerging competitive battleground aimed at improving shipper negotiating power relative to buyers. More shippers are investing in developing proprietary varieties with improved characteristics not just at the production level—yield and disease resistance—but also with improved consumer traits, such as flavor, size, shape, culinary characteristics or color. In a few instances, shippers offer their proprietary varieties on a selective or exclusive basis to key accounts as a market segmentation strategy and to support the retailer’s market differentiation and positioning strategy. As always, by introducing new dimensions of competition suppliers may increase bargaining power.

Some seed companies are partnering with shippers to grow and market proprietary varieties, such as the partnership between Syngenta and Dulcinea for specialty melons and tomatoes, including the Tuscan cantaloupe and PureHeart small, seedless watermelons. In general, vegetable seed firms are focused on developing more varieties with consumer traits, whether selling the seeds to the grower or operating in production partnerships with grower-shippers, as a strategy for capturing more of the downstream value of vegetable seeds. If well executed, these arrangements may also be beneficial to shipper bargaining power with key accounts.

As buyer bargaining power has grown, some commodity producers have become interested in the potential benefits of information-sharing cooperatives as a strategy for gaining countervailing power. Firms join cooperatives voluntarily, and once members, are legally permitted to share information on volumes and pricing with their competitors. For example, in the lettuce industry, California growers and shippers have attempted to improve their bargaining power through the Central California Lettuce Producers Cooperative. It enables firms to better plan flow to market largely through greater transparency on total member weekly volume available to sell.

Lettuce co-op members report learning a great deal about supply and demand in the lettuce market, thereby making them more effective at managing supply and indirectly, pricing and total returns. Since September 2006 when the cooperative began sharing information, FOB lettuce prices have largely remained profitable after frequent periods of losses in preceding years. The cooperative also attempts to achieve some discipline among members in negotiating forward contract pricing with buyers. Lettuce is one of the produce commodities most involved in forward contracting in part due to the important role of lettuce in retailer sales and on foodservice menus, making advance planning very important for buyers.

Recently, the orange, lemon, potato, mushroom and other commodity sectors have also been experimenting with information sharing cooperatives. However, firm rivalry and differences in marketing strategies of co-op members have frequently limited the success of this strategic response to growing buyer concentration.

The threat of new entrants in any industry always depends in part on current profit levels and the rate of growth in demand. Supply growth depends in large part on the flexibility of crops to adapt to different land conditions, climates and seasons, the distance to key markets of specific growing regions, whether or not the product is a perennial, the period of time to come into full production, the level of technology required, and the capital outlay per acre. Shelf-life, perishability, natural ethylene production and sensitivity, the ability of a product to withstand the rigors of the distribution system and other postharvest factors also play an important role. For example, leafy greens cannot be shipped easily with tomatoes, avocados, bananas and other ethylene producing/ripening crops since the former are susceptible to ethylene damage. For this reason, most shippers operate within commodity groups that can be successfully handled and shipped together and are not truly wide-line in the sense of operating across diverse fruit and vegetable categories.

Therefore, while demand varies by individual fruit and vegetable, the threat of new entrants tends to vary by commodity subsector since the pool of competitors at the shipping/marketing level is usually defined by subsector (for example, berries) rather than by individual crop. Grower-shippers in a commodity subsector are generally capable of developing production of any of the crops in that subsector if profit levels warrant entry. However, some specialization within a subsector will still tend to occur due to firms’ historical production patterns, land bases, know-how, risk preferences, varieties, and other factors affecting relative competitiveness. Each crop/subsector has its own story to tell in terms of the interaction of all of the forces for change.

The high level of production risk and price volatility at the produce grower and shipper levels does not encourage entry by publicly traded companies concerned with quarterly profit reports to shareholders. The main exceptions are multi-nationals anchored in the banana industry and Dole in particular—the only multinational wide-line fresh fruit and vegetable shipper operating in the U.S. market.

Today short-season growers outside of the main production regions are increasing production and selling more to retailers and to some restaurant segments as part of what are referred to as “local” buying programs, and gaining a small but growing share of the fresh produce market. USDA researchers estimate that local sales of fruits and vegetables surpass $3 billion through both direct-to-consumer and intermediated—to retailers and foodservice—channels (Low and Vogel, 2011). This trend has unfolded rapidly and is impacting the supply chain during the summer/fall when climate makes production possible in states with short growing seasons. Direct-to-consumer sales include sales through over 7,200 farmers markets nationally (USDA/AMS, 2011). Total fresh produce direct-to-consumer sales, excluding intermediated sales, likely represent less than 2% of the final value of the fresh produce supply chain or an estimated $1.4-1.8 billion in 2010.

Not all of this represents new entrants, since much of the above volume originates in the key production states. For example, California has over 700 farmer’s markets, many operating year-round, and the number of small growers has increased, many of which use farmer’s market channels. While new entrants are likely to continue, there are scale limitations to major growth in direct-to-consumer channels, just as climate limits longer production seasons in many states.

New entrants to the fresh tomato industry have been significant over the last two decades, and in the United States they have largely come from outside of agriculture in the form of greenhouse tomato operations. These capital-intensive businesses produce very high yields and offer higher value, differentiated tomatoes, such as tomatoes-on-the-vine, beefsteak and snacking tomatoes. According to retail scanner data, the round field tomato share of tomato sales declined from 43% in 1999 to18% in 2010. Round field tomato producers have been compelled to increase their reliance on sales through foodservice channels which have a preference for firm tomatoes that stand up to slicers. New entrants to this industry continue, in part due to interest from venture capitalists, further challenging the field grown tomato industry. There are even more new greenhouse vegetable entrants in neighboring Mexico, although in this case investment is from both inside and outside of agriculture.

The fresh produce industry is generally characterized by labor-intensiveness. However, it is also capital-, technology-, know-how-, post harvest handling-, service- and marketing-intensive. The United States tends to have advantages in these areas and firms substitute capital and technology for labor such that a given differential in hourly labor rates equates to a lower differential in labor costs per unit of production. Furthermore, transportation costs are an important share of fresh produce total costs upon arrival—landed costs—in destination markets. This frequently gives a landed cost advantage to domestic producers when in-season, even in cases where foreign producers do have a cost advantage at the point of initial shipment.

Nevertheless, U.S. industry members are concerned that their relative competitiveness is being eroded by the expansion of domestic regulations and threats to the availability of farm labor; thereby making them vulnerable to foreign competitors with export-oriented production. Still, firms face a more transparent legal system in the United States than in many other countries and benefit from robust infrastructure and agribusiness support structures, including federal and land-grant university research and extension. Due to all of the above, most fresh produce crops grown in the United States have remained competitive.

Exceptions are primarily for crops requiring bunching at harvest, such as asparagus, radishes, green onions and cilantro where labor costs are a higher share of total costs. Tomatoes are the other main exception, but in this case it is not due to a foreign cost advantage but rather to the ability of Mexico to offer differentiated vine-ripe or greenhouse tomatoes sold at a price premium relative to the dominant mature green tomato grown in the United States.

In short, numerous factors have influenced the number and location of new entrants by commodity, rather than a simplistic view of domestic versus foreign competition. However, as post harvest technology improves it may become feasible to ship products over even longer distances while maintaining acceptable quality, exposing the domestic industry to more potential competitors.

Substitution effects are quite pronounced in fresh produce, with consumers having many options and often substituting within and even across product categories based on the season, which in turn influences availability, appearance, flavor and price. The number of substitutes available in all seasons has increased markedly over the last two decades due to growth in: (1) domestic production and imports of specialty produce—Asian and Hispanic vegetables, for example; (2) product differentiation, such as, specialty apples, potatoes, sweet onions; (3) growth in winter imports of conventional fruits and vegetables—like table grapes, tree fruit, tomatoes, asparagus; and (4) year-round availability of tropical fruits.

Consumers today are more knowledgeable about the diversity and usage of fresh produce, with the average fresh produce department in supermarkets offering over 300 items. While some consumers have increased both the quantity and diversity of produce they purchase, many have merely made substitutions, such that traditional products like bananas, apples, pears, iceberg lettuce, carrots and potatoes have experienced stable or declining per capita consumption, while others such as tropical fruits, berries, chile peppers, colored bell peppers, and broccoli have increased. Health benefits as well as purpose and usage occasions influence substitutions.

Substitution also exists between fresh and the more economical processed fruits and vegetables, with the economic downturn contributing to at least a temporary increase in substitutions across these product forms. Substitutions have always taken place between many CPG items and fresh produce, such as salty snacks and sweets. Part of new product development in the fresh produce industry has focused on convenient RTE snacks designed to better compete with these items. However, the fresh-cut category in turn competes with and often cannibalizes commodity fresh produce sales.

In order to continue to drive non-value-adding costs out of the value chain, information technology must be applied much more intensively than in the past. This requires sizeable investments by firms at each level of the value chain, such as in Enterprise Resource Planning (ERP) systems and Customer Relationship Management Systems (CRMs). Firms creating data warehouses can readily access and analyze all aspects of their operations, thereby identifying opportunities for internal efficiency gains.

System-wide efficiencies may be realized if firms put in place systems that facilitate data sharing between vertical interfaces of the value chain, such as shipper to retailer. Retailer reluctance to share information with suppliers has been a barrier to wider adoption of business intelligence practices, but this is changing. More executives understand that the new competitive paradigm requires still greater vertical coordination and collaboration between buyer and seller in order to better serve consumers, which in the final analysis is the key to competitiveness. However, while today more retailers share data, many charge for it, a barrier that limits progress.

As cutting-edge suppliers begin providing marketing and promotional support to retailers, it becomes critical to engage in the complex process of analyzing promotional efficiency and to develop concrete metrics to ensure that expenditures and tactics provide a positive return on investment for both the buyer and seller.

Similarly, shrink—physical product losses—may be reduced through information sharing. While total fresh produce system-wide shrink is unknown, retail shrink is often in the order of 6% and estimated total annual losses may reach approximately 10% of the produce chain final value, equivalent to $12 billion. Better information management systems would contribute to a higher probability of getting the right product to the right store, offering an enormous opportunity for lowering shrink and for system-wide efficiency gains, including in transportation and logistics. Retailers succeeding in shrink reduction are better able to maintain margins without raising prices. Buyers and sellers succeeding in this new arena may gain stronger relationships and improve competitiveness in their own market segments, making these efforts mutually beneficial and strengthening buyer-seller loyalty.

Purchasing information technology is costly and these investments will likely drive further increases in firm size. Recently, investments at the shipper level have arguably been slowed more by lack of ERPs that work well for fresh produce firms, than by lack of shipper interest. At the retail level, the economic downturn has slowed investment in improved technology and few retailers have fully tapped the potential consumer insights available from mining their consumer loyalty card data. Yet the economic downturn has also brought home to all fresh produce industry actors that margin squeeze is likely to continue for some time and that these investments are essential to productivity gains. Firms are recognizing that there are many opportunities for efficiency gains that were simply overlooked until the economic downturn imposed a new competitive benchmark. This is true regardless of firm type or size.

These trends are unfolding just as mobile technology is becoming a more viable way to reach consumers cost-effectively through opt-in programs, including customized in-store mobile promotions and instantaneous consumer access to product information—for example, through Quick Response (QR) codes. In addition, the potential opportunities and challenges of social media are just beginning to unfold in the fresh produce value chain. As smart phone adoption rates grow, mobile platforms and social media will likely become more closely intertwined as part of the consumer engagement strategies of both fresh produce firms and retailers. Advances in technology can be disruptive and alter products and services demanded by others in the value chain, making this new arena important to marketing strategies and tactics.

Speed in the identification of winning consumer marketing strategies may be a factor affecting firm level competitiveness going forward. With the rapid rate of change in the food industry, speed is becoming more important in all arenas, and those making effective use of information technology will likely be more nimble in both identifying opportunities and addressing challenges.

As essentially consumer ready products, fresh fruits and vegetables are on the front lines of evolving consumer food trends. One of the most important drivers of change in recent years has been consumer interest in where and how food is grown and greater demand for transparency and responsible business practices throughout the value chain, all part of what is often referred to as values-based food systems. Fresh produce has benefited from its positioning as natural and healthy but has been subject to serious microbial food safety incidents that can, at least temporarily, threaten this positioning. In addition, the Environmental Defense Fund annually publishes a “Dirty Dozen” list of fruits and vegetables that allegedly have pesticide residues that may pose health concerns to consumers. Despite scientific evidence to the contrary, about 40% of U.S. consumers believe that pesticide residues on food pose a significant health risk (Food Marketing Institute, 2011).

Various factors have contributed to rapid growth in demand for organically grown fresh produce, which is a leader within the organic foods category and a point of entry for consumers as they explore participation in this market. Three-quarters of U.S. consumers purchase organically grown foods at least periodically and, based on Nielsen retail scanner data, the estimated contribution of organic fruits and vegetables to the average fresh produce department’s sales is 5%, and growing. Approximately 18% of households are described by the Hartman Group as core consumers or frequent buyers of organic foods. This segment also tends to be one of the highest consumers of fresh produce in general, both conventional and organic. Many of these consumers are very engaged in the politics of food and increasingly express their opinions through social media, which can rapidly impact the views of opinion leaders.

For example, this consumer segment tends to be a leader in calling for “sustainability” in farming and distribution practices, generating increased consumer interest in “local sourcing,” discussed earlier. Local products are frequently perceived to be more sustainable and safer than produce grown in distant locations, often by large producers. The latter are frequently framed in a negative light with the term “corporate farming,” despite the fact that most produce growers and shippers are family-owned firms, usually multi-generation, regardless of location. Production in the major growing locations for specific crops may utilize fewer resources than short-season production outside of these areas due to a variety of factors which affect yields and cost structures, even including transportation costs to market. Nevertheless, consumer demand is growing and provides exciting opportunities for growers in short-season locations.

The perception of freshness is driving consumer demand for food in general, with many consumers interested in consuming foods perceived as “less processed,” clearly benefiting fresh produce. In addition, the foodservice industry continues to increase menu placements of fresh produce. For the fast food industry, negative consumer attitudes about its potential contribution to the U.S. obesity crisis should continue to drive new product introductions. Food service firms are also changing the default options toward healthier fresh produce items, such as apples in McDonald’s Happy Meals.

There are numerous changes in public policy which are acting as positive drivers of change for both short-term and long-term fresh produce consumption. These include the importance of fruits and vegetables in our diets as outlined by the new federal dietary guidelines MyPlate, which recommend that half the plate be fruits and vegetables. In addition, there is rising federal funding for fresh produce purchases, including: produce served in meals and snack programs in schools, and in the Supplemental Nutrition Assistance (SNAP) and Women, Infants and Children (WIC) programs; the addition of salad bars to schools, often through public-private partnerships; and awareness-building programs of the benefits of diet and exercise, such as First Lady Michelle Obama’s Let’s Move Initiative to combat childhood obesity. The Produce for Better Health Foundation (PBH), United Fresh, and the Produce Marketing Association have played a leading role in stimulating public policy change. PBH also has active online consumer communication programs, including utilizing social media, and is targeting Gen X and Gen Y mothers with tools for including more fruits and vegetables in their family’s diets.

Food safety is a significant driver of change in the fresh produce industry. Food safety risks from consuming fresh produce are extremely low but, unlike animal products, they are often consumed raw. Since there is no “kill step” before consumption, management of the risk of food-borne pathogens is all important if fresh produce is to retain the healthy halo effect that it now enjoys—and rightfully so according to an expanding base of scientific research. Given that most fresh produce is grown out-of-doors, it is impossible to eliminate risk but firms are aggressively attempting to mitigate risk. For some time, commercial growers have been investing in improved food safety processes, despite the lack of many mandatory government standards. This has unfolded based on buyer requirements and industry interest in following Good Agricultural Practices in order to provide a wholesome, healthy product.

This more market-based approach is set to change in light of the Food Safety Modernization Act of 2010 (FSMA), part of which has already entered into effect through U.S. Food and Drug Administration (FDA) regulations. The development of many important regulations is still in process, making the potential impacts of the Act as yet unknown. It is expected to somewhat level the playing field in terms of requirements. Whereas currently some buyers may still source part of their needs from firms with lower investments in food safety—occurring more frequently in short markets—in the future all suppliers must meet the same standards.

Traceability is already being improved with the one-step forward, one-step back approach, and advances in technology and industry practices should facilitate traceability value chain-wide. Numerous newly emerging firms are offering mobile scanning technology and systems that identify and link product from the field through distribution. In 2006, produce leaders through their trade associations established a Produce Traceability Initiative (PTI) to work toward system-wide traceability at the carton level. Firms have developed internal traceability and the PTI uses a Global Trade Item Number (GTIN) to achieve external traceability. Various pilot projects are underway to develop best practices and the PTI administering organizations are working with the FDA on an ongoing basis.

Sizeable investments in food safety research are being made via public-private-academic partnerships such as the Center for Produce Safety at the University of California, Davis. As the science supporting food safety improves, it should be more feasible to target practices most efficient in mitigating risk and preventing outbreaks, as well as to increase the efficiency of monitoring, verification and enforcement systems. As the scientific experts routinely note, you cannot test your way to food safety. In the meantime, increased concern by regulatory agencies about food safety risk in fresh produce has led to an expansion in microbial testing by the government, which is supplementing the mounting testing requirements of many buyers.

The food safety practices and procedures of the larger growers and shippers are verified by third party auditors. Often, shippers are required to pay for the services of numerous third party auditors due to the verification policies of specific retail and foodservice customers. This involves significant duplication and redundancy. If the new regulations were to standardize verification requirements, costs should decrease and it would free up these expenditures for investment in areas with greater potential for actual risk mitigation.

It is the larger growers that have the most wherewithal to invest as the costs per box attributed to food safety standards continue to rise. This poses special challenges to many smaller growers which have yet to meet the standards already implemented by the firms marketing the majority of supply. An exemption for some smaller growers is included in the Tester amendment of the new FSMA, based on various marketing criteria—marketing channels, shipping distance, size—rather than on science-based criteria related to actual food safety risk. This remains extremely controversial with many fresh produce stakeholders. However, regardless of government regulations, commercial buyers have been raising standards and smaller growers that want to sell outside of direct-to-consumer channels should expect to make further investments in food safety practices. This may contribute to an increase in average firm size in short-season production regions. The speed of change is high, and the depth and breadth of the responses needed to adapt to these changes is likely to be substantial.

Another driver of change that could impact firms throughout the produce industry and beyond is E-verify, once implemented nationally—in some states, such as Arizona, it is already implemented. It is estimated that the fresh produce industry relies on undocumented workers for a majority of its labor supply and other sources of labor are not available, given the difficult working conditions required to grow and harvest fresh produce. In general, the federal government is becoming much more active in regulating and policing labor and housing practices in the produce industry. Growers expect some type of temporary farm worker program to emerge eventually from Congress to address the vital need for seasonal workers, but this outcome is far from certain.

If labor availability were to be seriously constrained, supply adjustments could be significant. Mechanization of fresh fruit and vegetable harvesting is much more challenging than for processed forms due to quality requirements and characteristics of fresh market varieties, certainly in the short-term. In addition, production of many crops cannot be easily shifted off-shore during U.S. growing seasons. Where necessary and feasible to move off-shore, U.S. firms would lead the way and continue to control marketing of the crops. However, there would be a major adverse effect on growers, who are tied to the land. Those firms that most rapidly adapt to a reduction in labor supply would be major gainers in market share. On the other hand, it seems unlikely that policy makers will in the end stand by while potentially half of fresh produce workers are lost, given the important implications for food costs and jobs.

The twenty-first century U.S. fresh fruit and vegetable marketing system has strengthened its focus on adding value and decreasing costs by streamlining distribution and understanding customer/consumer needs. The economic downturn is emphasizing the need for further gains in efficiency and has increased the speed of change. Some firms are adapting more quickly than others, causing rapid changes in relative competitiveness and firm level positioning strategies. Speed can increasingly provide a competitive advantage.

Growing regulatory, food safety, technological, new product development, and marketing requirements are increasing fixed costs for fresh produce suppliers and the need to generate higher volumes over which to spread these costs. Therefore, there are strong incentives for further supply side consolidation and these combined forces are increasing both barriers to entry and exit. Retailers will continue to face channel blurring and margin pressure. The incentives for closer collaboration between suppliers and buyers are mounting and collaborative relationships are increasingly recognized as an important component of firm level strategy.

Bluebook online queries. (June 2011). http://apps.bluebookservices.com/BBOS/Login.aspx?ReturnUrl=%2fbbos%2fDe fault.aspx. Access through paid subscription.

FDA. (2010). Food Safety Modernization Act of 2010. Available at: http://www.fda.gov/food/foodsafety/fsma/default.htm.

Food Marketing Institute. (2011). U.S. grocery shopper trends 2011.

Low, Sarah A., and Stephen Vogel. (2011). Directand intermediated marketing of local foods in the United States.ERR-128. Washington, DC: U.S. Department of Agriculture, Economic Research Service, November 2011.

Olson, K. and Boehlje, M. (2010). Theme overview: fundamental forces affecting agribusiness industries. Choices, 25(4).

Nielsen/Progressive Grocer. (2010). Marketing guidebook: the comprehensive source for grocery, drug and mass merchant insights.

Planet Retail online queries. (2011). http://www.planetretail.net. Access through paid subscription.

Porter, Michael E. (2008). The Five Competitive Forces that Shape Strategy. Harvard Business Review, January 2008, 79-93.

The Food Institute. (2011). The food institute report, 84th Year No. 25, June 27, 2011.

U.S. Department of Agriculture, Agricultural Marketing Service (USDA/AMS). (2011). Available at: http://search.ams.usda.gov/farmersmarkets/.

U.S. Department of Agriculture, Economic Research Service (USDA/ERS). (2011a). Fruit situation and outlook yearbook, October 2011.

U.S. Department of Agriculture, Economic Research Service (USDA/ERS). (2011b). Vegetables and melons yearbook data, May 2011.

U.S. Department of Agriculture, Foreign Agricultural Service (USDA/FAS). (2011). Online queries at: http://www.fas.usda.gov/gats/default.aspx.

U.S. Department of Agriculture, National Agricultural Statistics Service (USDA/NASS). (2011). Vegetables 2010, January 2011.